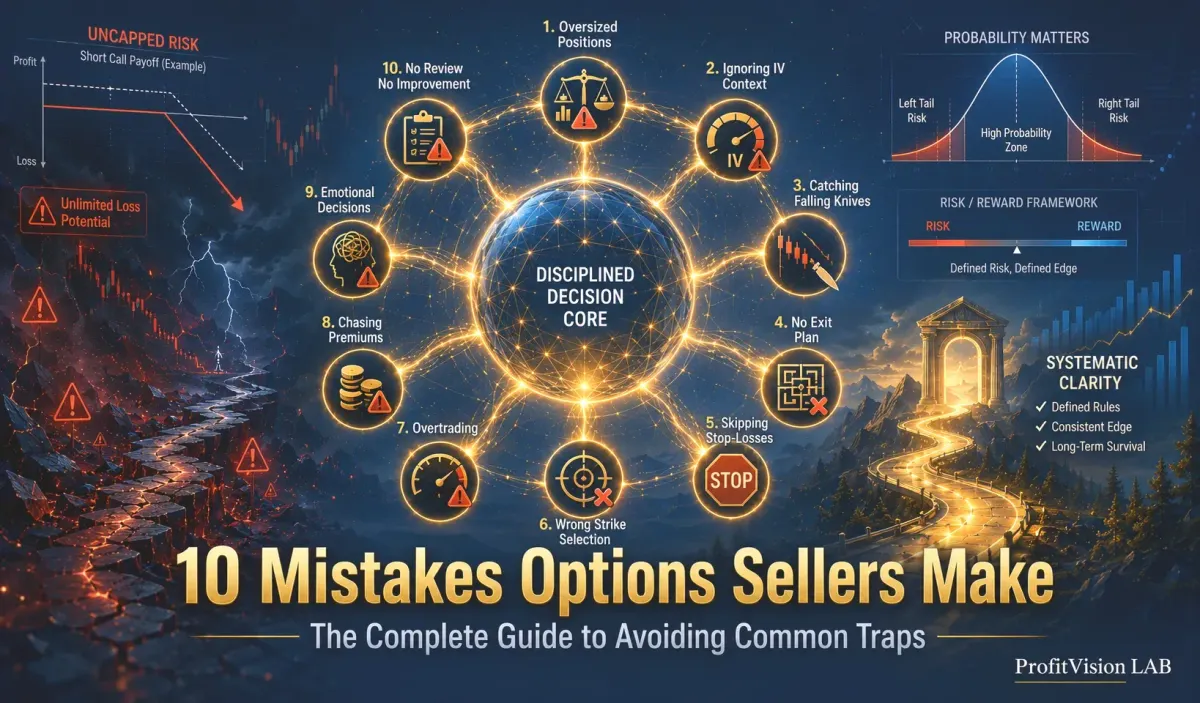

10 Mistakes Every Options Seller Makes (And How to Fix Them)

Options sellers have a mathematical edge — but only for systematic, disciplined practitioners. These are the 10 most common mistakes that neutralize that edge, each with real scenarios and concrete fixes.

- Options sellers have a mathematical edge — time value erodes daily, probability favors the seller. But this edge only works for systematic, disciplined practitioners. The mistakes beginners make are precisely the ones that neutralize this structural advantage.

- The most dangerous mistake is #1 — believing options selling is a "sure thing." That cognitive error is the root cause of every other mistake on this list.

- Every mistake below comes with a real-world scenario and the correct approach — so you can immediately check your habits against what you read here.

- If you haven't started options selling yet, this is the best preventive medicine. If you've started but keep bleeding small losses, this article probably names your problem.

Why Do Options Selling Beginners Start Strong, Then Watch It Fall Apart?

Options selling has an addictive quality for newcomers: the first few trades almost always work. Premium collected, contract expires worthless, repeat. The "beginner's halo" can last months — then one outsized loss erases everything you earned, and then some.

This isn't a flaw in the strategy. It's because beginners spend those months doing one thing: repeating actions that feel effective, without first building the risk framework that makes those actions sustainable.

The 10 mistakes below aren't hypothetical. They are real loss patterns that recur again and again in real accounts. If you recognize yourself in this list, congratulations — you still have the chance to fix the system before it collapses.

The deepest psychological trap for sellers is that premium looks like "guaranteed income" while the loss looks like "something that probably won't happen." But options are structurally asymmetric: the buyer's maximum loss is the premium paid (finite), while a naked seller's maximum loss — in theory — is the stock going to zero.

This doesn't make selling a bad strategy. In the majority of outcomes, it works. But you must first genuinely internalize this: a single black swan event can wipe out six months of premium income and go beyond. Accepting that reality is the prerequisite for designing the right risk system.

Oversizing is one of the most common beginner errors. When a single trade consumes a large portion of your account, any temporary adverse move creates massive psychological pressure — pushing you toward emotional decisions at exactly the wrong moment.

The deeper problem: even if your direction is ultimately correct, the volatility in between may force a premature exit at the worst possible price. You were right about the stock; you just couldn't survive long enough to collect.

Options selling is fundamentally the business of selling volatility insurance. When IV is very low, the market expects little future movement — your premium is correspondingly small. But low IV doesn't mean the stock won't move. It just means you're accepting huge downside for tiny compensation.

When IV Rank breaks above 80%, the market is almost always pricing in a real, known bad event. Selling Puts in that environment — attracted by the fat premium — is catching a falling knife. Every level you think is a bottom has another floor below it.

High IV is usually there for a reason — the market sees elevated risk in this stock and is willing to pay high premiums for protection. For a buyer, this is a directional bet. For a seller, it should be a warning signal, not a yield opportunity.

Companies with poor fundamentals (chronically negative ROE, declining EPS, institutional distribution) don't deserve a seller's capital regardless of how elevated their IV is. "High IV plus bad fundamentals" almost always means the market has already identified the problem — and you are providing liquidity for that judgment at your own expense.

Trying to call the bottom is a natural human instinct — and in markets, it's a near-certain losing strategy. A stock in a confirmed downtrend typically falls further and longer than you expect. The 50-day moving average exists precisely to solve this problem — it provides an objective measure of "is the trend intact?" rather than relying on gut feeling.

Price below the 50MA signals a medium-term downtrend. Selling Puts in that environment is fighting the trend. Even a fundamentally excellent business should be left alone until the trend confirms a reversal — patience here prevents far larger losses.

Professional options sellers widely use a rule: close the position when you've captured 50% of the premium. The logic is clear: after collecting 50%, the remaining 50% doesn't justify continued holding through to expiration. As expiration approaches, Gamma risk accelerates — each $1 move in the stock creates an increasingly large impact on your option's value. Your risk exposure actually increases as DTE decreases, not the other way around.

① Profit target: Close when the option's value falls to 50% of the original premium received (you've captured 50%). Don't be greedy waiting for full expiration.

② Stop-loss: Close when the position's paper loss reaches 2–3× the original premium received (e.g., collected $3 premium → exit when loss reaches $6–$9). Small losses must not be allowed to become large ones.

Before earnings, uncertainty about the future is at its peak — IV inflates artificially. That's exactly why the IV Rank looks attractive. The problem is that earnings are a binary event (beat/miss), and even with a correct view, there's roughly a 50% chance of a gap move that exceeds your Delta cushion and collected premium. Earnings gaps don't care about your strike level.

After earnings, IV typically collapses sharply — this phenomenon is called "IV Crush." That post-earnings environment is the correct time to enter: lower premium than pre-earnings, but the biggest single risk catalyst is gone.

① Skip the trade entirely — wait for earnings to pass, then re-evaluate;

② Only open positions after the earnings print, harvesting normalized IV in the post-Crush environment.

The 30–45 DTE window is optimal for options sellers for a specific structural reason: this range sits in the "sweet spot" of Theta decay. Time decay accelerates as options approach expiration, but so does Gamma — the rate at which your delta (and therefore P&L) changes with each dollar of stock movement. Very short DTE positions give up this tradeoff, concentrating Gamma risk into a small window while offering disproportionately thin premium as compensation.

By contrast, 30–45 DTE positions have had enough time for Theta to meaningfully erode the option while keeping Gamma at a manageable level. If the stock makes a short-term adverse move, you have time and buffer to manage the position rather than immediately being forced to cut.

Options selling is a family of strategies, not a single technique. Each member of the family has a specific applicable context:

- Naked Short Put: Bullish, sufficient margin, willing to be assigned stock at the strike

- Bull Put Spread: Bullish-to-neutral, smaller account, defined maximum loss preferred

- Covered Call: Already holding 100 shares, want to reduce cost basis

- PMCC (Poor Man's Covered Call): Bullish but don't want to buy 100 shares — use a LEAP as a synthetic substitute

For accounts under $10,000, the Bull Put Spread is the ideal starting strategy — maximum risk is precisely defined before entry, no large margin commitment required, strategy logic is clean and executable.

The mathematical edge of options selling comes from the law of large numbers — over a sufficient number of trades, the probability advantage begins to express itself and compound in the account. But this requires time, and throughout that time, it requires emotional consistency.

Two most common emotional traps for beginners:

- Tailwind overconfidence: After a run of winners, believing you've "found the secret" and doubling down — then suffering amplified losses when the inevitable adverse cycle arrives

- Headwind capitulation: After a significant loss, concluding the strategy is broken and abandoning the system entirely — often at the moment when IV is highest (market most fearful), which is historically the best environment for options sellers

Summary: The 10-Mistake Quick Reference

Disclaimer: All content in this article is for research and educational purposes only and does not constitute investment advice. Stocks, ETFs, and strategies mentioned are used to illustrate concepts, not to suggest any buy or sell action. Options trading involves substantial risk. Selling options strategies can result in losses significantly exceeding the premium collected. Investors should assess their own risk tolerance and make independent decisions accordingly.

Comments ()