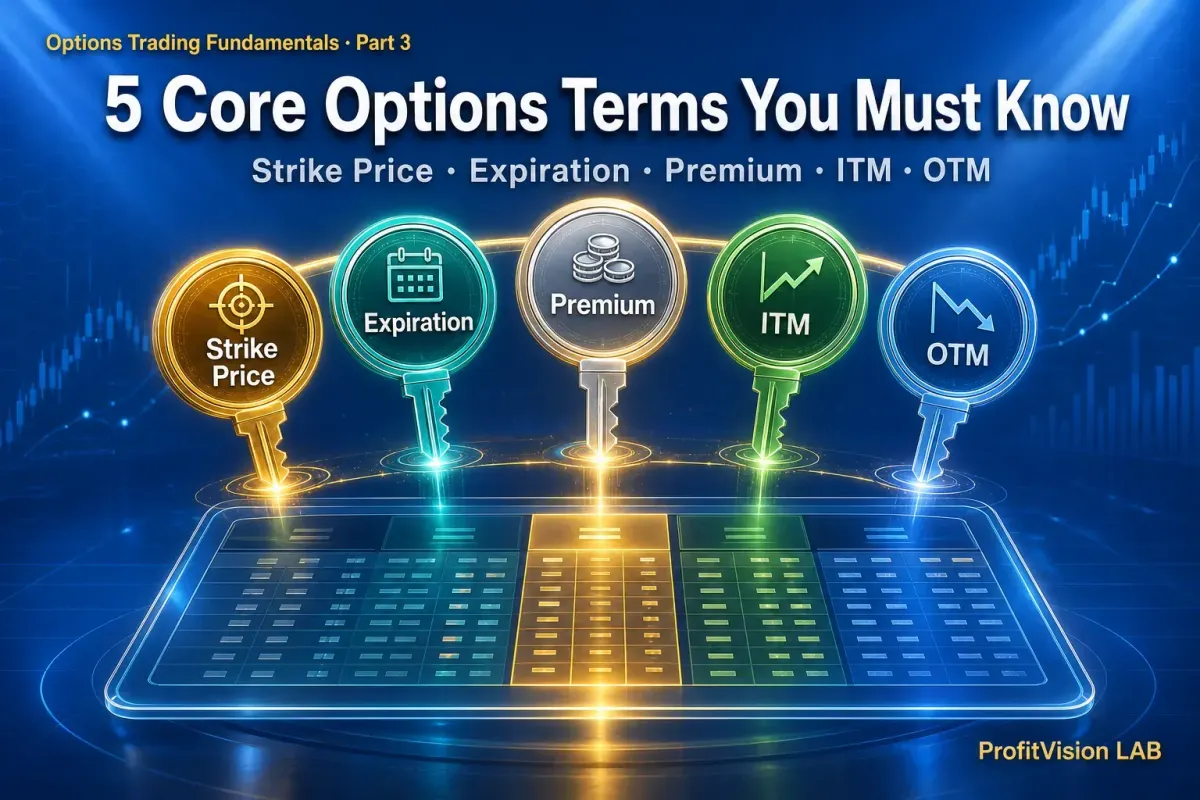

5 Core Options Terms Every Investor Must Know

Before placing your first options trade, five terms determine whether you know what you're doing: strike price, expiration date, premium, in-the-money, and out-of-the-money. This guide explains each with real options chain examples — so you never misread a contract again.

- There are five core options terms you must understand: Strike Price, Expiration Date, Premium, In-the-Money (ITM), and Out-of-the-Money (OTM)

- The strike price defines your "line in the sand"; the expiration date sets your time pressure; the premium is the cost you pay or the income you collect

- ITM / ATM / OTM describe the relationship between the strike price and the current stock price — for the options seller, choosing an OTM Put means there's a buffer zone between where the stock trades now and where your obligation begins

- By the end of this article, you'll be able to read every column on an options chain without confusion

🔑 Terminology Is the Key to Unlocking Options

Most beginners freeze when they see an options chain — Bid, Ask, Strike, Exp, Delta, IV... a wall of abbreviations. But here's the truth: master just five core terms and you'll be able to decode 80% of the information on any options chain. The rest you can pick up through practice.

The approach in this article is simple: one clean definition per term, followed by one concrete example to lock it into memory.

Every term carries a very specific, real-world meaning — once you understand the underlying concept, you'll find the naming remarkably intuitive.

🎯 Term 1: Strike Price

For Put sellers, the strike price is your "line of defense": you're committing to buy shares at that price if the stock falls to or below it by expiration. The lower the strike you choose relative to the current stock price, the more cushion you have — but the lower the premium you collect in return.

⏳ Term 2: Expiration Date / DTE

The expiration date is the single biggest structural difference between options and stock ownership. Owning stock carries no time pressure — but options contracts are constantly burning through time. DTE (Days to Expiration) is one of the first numbers you'll notice on any options chain.

For options sellers, the 30–45 DTE window is the sweet spot: long enough for Theta decay to work steadily in your favor, yet short enough to avoid prolonged exposure to uncertainty.

💰 Term 3: Premium

Premium is determined in real time by the market and is influenced by three primary factors:

- Time remaining: The more time until expiration, the higher the premium — more time means more opportunity for the unexpected to happen

- Distance from the strike: The closer the strike is to the current stock price, the higher the premium — the probability of exercise is greater

- Implied Volatility (IV): The higher the market's expectation of future volatility, the higher the premium — more uncertainty means higher demand for options as insurance

Premium is quoted on a per-share basis, and one standard contract represents 100 shares. So a quoted premium of $3.00 translates to $3.00 × 100 = $300 in actual cash received or paid.

📍 Terms 4 & 5: In-the-Money, At-the-Money, Out-of-the-Money (ITM / ATM / OTM)

These three terms describe the relationship between the strike price and the current stock price — a critical factor for sellers when selecting which strike to use.

From the seller's perspective: selling an ITM Put means your chosen strike is already above where the stock is trading — the stock has effectively already breached your line of defense. ITM options carry the highest premiums, but they also carry the highest assignment risk. You will very likely be forced to buy shares.

From the seller's perspective: OTM Puts are the natural territory of the options seller. The strike you've chosen is below the current stock price, giving you a buffer zone before your obligation kicks in. Premium is lower than an ITM option, but the probability of assignment is significantly reduced.

ProfitVision LAB typically targets OTM Puts with a Delta of 0.20–0.30, meaning the stock has roughly a 70–80% probability of expiring above the strike price and the premium is collected in full.

📊 Putting It All Together: Reading a Real Options Chain

Imagine you're looking at the following data on IBKR's options chain for AAPL (stock price $200, 45 days to expiration):

📌 What is OI (Open Interest) — and why does it matter?

OI (Open Interest) represents the total number of outstanding contracts that have not yet been settled. Higher OI means better liquidity at that strike — easier to enter a position and exit when needed. This metric is often overlooked by beginners who focus only on the premium amount.

A common rookie mistake: chasing a juicy premium on a strike with very low OI. If there are only a few dozen open contracts, you might be able to open the trade, but closing it at a fair price becomes a real challenge — you're walking into a wide bid-ask spread or no counterparty at all. As a general rule, look for OI of at least 500 contracts before entering a position.

👤 Seller's Perspective

AAPL is at $200. The seller picks the $180 Strike (Delta 0.18, OI 4,200) — the stock would need to drop 10% ($20) before reaching your strike. You collect Bid $1.40 (= $140 in premium), your probability of profit is approximately 82% (the stock has an 82% chance of staying above $180 at expiration), and OI of 4,200 provides ample liquidity. This is the classic options seller setup.

👤 Buyer's Perspective

Same chain, different angle: you expect AAPL to sell off and want to use the $190 Strike Put (Delta -0.30, OI 5,100) to hedge or make a directional bet. You pay Ask $3.50 (= $350 in premium) for the right to sell AAPL shares at $190 if the stock falls below that level.

The buyer's breakeven: $190 − $3.50 = $186.50 — the stock needs to fall below this level before you're in profit at expiration. For the buyer, direction must be right, the move must be large enough, and it must happen fast enough — otherwise Theta erodes your premium a little more every day.

Options markets move fast — Bid, Ask, OI, and IV are all changing by the second. Trading on delayed quotes is like navigating with a blindfold. For guidance on choosing the right real-time data tools and subscription plans, see: How to Read Your First Options Chain →

Core philosophy: "I teach you how to think, not just what to do."

Disclaimer: All content in this article is intended for research and educational purposes only and does not constitute investment advice. Options trading involves substantial risk of loss. Investors should assess their own risk tolerance and make independent decisions accordingly.

© 2026 ProfitVision LAB · Shiba the Disciplined · I teach you how to think, not just what to do

Comments ()