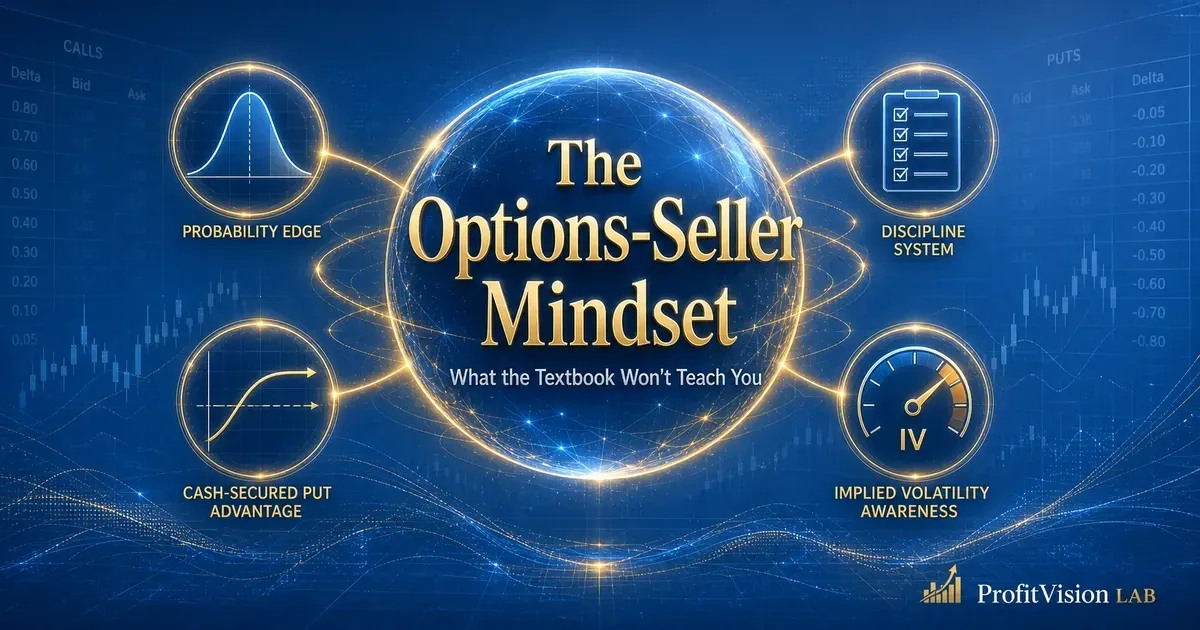

What the Textbook Won't Teach You: The ProfitVision LAB Options-Seller Mindset

Stop predicting direction. Start collecting premium. The options-seller mindset shift the textbook skips.

- 90% of options books on the market teach the buy side. PVL teaches the sell side — the two stand on opposite ends of every trade.

- The core of the options-seller mindset: stop predicting direction, and instead choose which of two acceptable outcomes happens first.

- Pick the right underlying and enter when IV is elevated — and the psychological pressure of selling options is far lighter than most people imagine.

- Using AAPL and NVDA as live examples: a Cash-Secured Put can generate an annualized return of 16–40% in a single month. The worst-case outcome is buying a stock you already wanted — at a discount.

Most people who discover ProfitVision LAB have the same first reaction: "Wait — this is nothing like what I read before."

That feeling is exactly right. Roughly 80–90% of options books on the market teach buyer logic. What I teach here is seller logic. The difference isn't a matter of style — the two sides stand on fundamentally opposite ends of every trade.

Do You Want to Be the Gambler — or the House?

Textbooks love to show that seductive diagram: "Pay $1,000 in premium, gain unlimited upside." It sounds beautiful. What they leave out is that stocks spend roughly 70% of the time going sideways, and every day that passes erodes the value of a long option contract. You think you're turning a small bet into a big win. In reality, you're paying tuition every single day to the seller on the other side of the trade.

The logic I teach runs the other way: instead of predicting whether a stock rises or falls, sell insurance and collect the premium. As long as the market doesn't suffer a major shock, the premiums paid by retail buyers flow straight into your pocket as consistent income. High win rate, steady rhythm — this is the house's business model, not the gambler's mindset.

Why Options Sellers Don't Need to Predict Direction

Conventional books spend enormous page counts teaching technical analysis — MACD, Bollinger Bands, candlestick patterns — all in service of predicting "will the market go up or down tomorrow?" That is not something I do, and it is not something I teach.

What I watch is IV (implied volatility). The logic is straightforward: when the market panics and bad news floods the tape, insurance premiums get pushed to irrationally high levels. Entering at that point to sell overpriced insurance — collecting premium that has been inflated beyond fair value — is a "buy low, sell high" business logic. It is not fortune-telling.

Is Options Trading a Gambling Tool or a Portfolio Management Tool?

Conventional books treat options as a standalone leverage instrument — no stock position required, pure magnification of a directional bet. Get the direction wrong and the premium goes to zero.

The PVL system ties options directly to the U.S. large-cap stocks you already intend to hold long-term. In a worst-case scenario there is no blow-up — only being obligated to buy the stock you planned to own anyway, at the discounted strike price you set in advance. That is not a risk; it is part of the plan.

Cash-Secured Put Live Simulation: AAPL vs NVDA

Using prices from late May 2026 as a reference, here is a direct simulation of PVL's opening strategy: the Cash-Secured Put (CSP).

Core idea: set a discounted price you are willing to pay. If the stock never drops to that level, you collect the premium as income. If it does drop there, you buy into a quality company at a discount you chose beforehand.

Example 1: Apple (AAPL) — The Steady Premium Collector

- Current market price: ~$312

- Target entry price: $290 (~7% discount)

Sell 1 AAPL Put | Strike $290 | 30-day expiration

Collateral locked: $29,000 ($290 × 100 shares)

Premium received immediately: ~$400 — credited the moment the order fills

AAPL closes above $290 → contract expires worthless, $400 premium is yours, $29,000 collateral is released

30-day annualized return: ~16.5%

AAPL drops below $290 → assigned 100 shares at $290; net the premium, your

effective cost basis: $286 — a ~8% discount to market

Example 2: Nvidia (NVDA) — High Volatility, High Premium

- Current market price: ~$214

- Target entry price: $190 (~11% discount)

Sell 1 NVDA Put | Strike $190 | 30-day expiration

Collateral locked: $19,000

Premium received immediately: ~$700 — IV is elevated, so the premium is especially rich

NVDA closes above $190 → $700 collected cleanly

3.6% in one month, annualized above 40%

NVDA crashes to $180 → after netting the premium,

effective cost basis: $183 — saving $30+ vs. chasing at $214

Pick the Right Stock, Time IV Correctly — and the Pressure Is Lighter Than You Think

Many people assume options selling carries enormous stress. In practice, this intuition is backwards. What truly keeps traders up at night is never the strategy itself — it is selling on the wrong underlying at the wrong time.

Virtually all psychological pressure in options selling traces back to two mistakes: selling a put on a stock you have no desire to own, or entering when IV is near its lows, collecting a thin premium that doesn't justify the risk.

But if you get two things right — only sell puts on quality large-cap names you already plan to hold long-term, and only enter when IV is elevated and the market is fearful — the entire psychological experience changes.

When Outcome A happens, you collect the premium and feel calm. When Outcome B happens, you acquire a stock you wanted anyway at a discount, and you still feel calm.

You are not gambling on an uncertain outcome. You are choosing which of two outcomes — both of which you can live with — happens first.

The low psychological pressure is not luck. It is the result of thinking everything through before you ever place the trade.

Now focused on U.S. options sell-side strategies, applying a systematic framework to screen underlyings and manage risk. The investment methodology integrates CANSLIM & SEPA stock-selection discipline, a four-filter entry standard, and Bull Put Spread position management — building a repeatable operating system grounded in the structural edge of probability and time.

Core belief: "I teach you how to think, not just what to do."

Comments ()