Ondas Holdings (ONDS) Deep Research Part 2: The $1B Predatory Playbook — Ondas Capital's Technology Bridge Rewrites the DefTech Map

Ondas Capital buys Eastern European battlefield-proven tech at wartime discounts, removes Chinese components for NDAA compliance, then monetizes at U.S. defense premiums. The $982M Mistral IDIQ validates the playbook. Information asymmetry as a systematic investment edge.

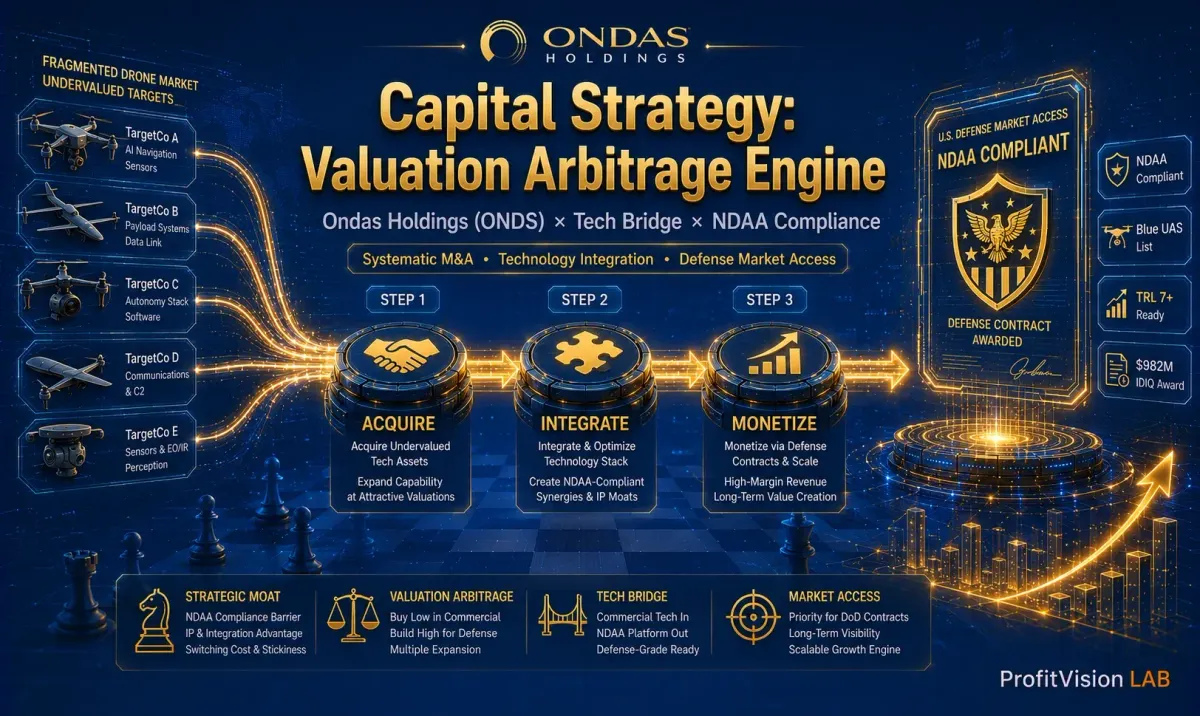

How Ondas Capital's $1B war chest deploys the Technology Bridge playbook — acquiring battlefield-proven technology at wartime discounts, achieving NDAA compliance, and monetizing at U.S. defense premium valuations.

2026.05.17 | Shiba the Disciplined | ProfitVision LAB | Last Updated: 2026.05.17 | Est. read time: 12 min

I. The Technology Bridge — A Three-Step Valuation Arbitrage Machine

The geopolitical backdrop matters here. Ukraine and Israel, operating in active conflict environments since 2022, have produced an extraordinary volume of battle-tested autonomous defense technology that is simply unavailable in American laboratories. Ondas Capital has built a systematic process to monetize this gap:

TRL 7+ battlefield-

verified technology

NDAA compliance

U.S. manufacturing cert

Federal procurement access

Valuation multiple jump

Technology Readiness Level (TRL) is the U.S. DoD's standardized scale (1–9) measuring how close a technology is to field deployment. TRL 7 means the system has been demonstrated in an operational environment — real battlefield or equivalent — not just a lab. TRL 9 is full system deployment.

Ondas Capital's TRL 7+ mandate is a disciplined risk filter: by only investing in technologies already validated under real conditions, the company eliminates the risk of fundamental technology failure. This compresses the time from "acquisition" to "revenue-generating deployment" — the key driver of Ondas Capital's returns.

The core insight is this: Eastern European technology companies operate in extreme wartime urgency but lack access to U.S. procurement channels. The U.S. DoD needs battle-proven systems but lacks visibility into what's being field-tested in Eastern Europe. Ondas Capital sits at the intersection of this information asymmetry — and charges the arbitrage spread.

II. The $1B War Chest — Deployment Priorities

The capital is not deployed randomly. Ondas Capital operates a strict investment hierarchy:

Strategic Acquisitions (M&A) — Immediate Revenue Contribution

First priority: targets that can immediately contribute revenue, are technically complementary, and priced at reasonable valuations. Key examples from the initial deployment wave:

- Roboteam: Brings an unmanned ground vehicle (UGV) platform into the group, filling the capability gap in ground autonomous operations.

- Sentrycs: Strengthens counter-drone (C-UAS) "protocol hijacking" capability — acquiring global critical infrastructure protection contracts, including Davos Forum and 2026 FIFA World Cup deployments.

- Iron Drone: Adds "hard-kill" interception capability, forming a layered defense pairing with Sentrycs' soft-kill approach.

Strategic Investments and Incubation — Building the Next Asset Cohort

Ondas Capital targets approximately $150M for direct investments in mature frontier technologies:

- Drone Fight Group (DFG): Investment of up to $11M, plugging the group's prior gap in "kinetic strike" (loitering munitions) capability — giving Ondas a complete "reconnaissance → intercept → strike" full-spectrum solution.

- Rift Dynamics: Strengthens low-cost, attritable drone deployment in Northern Europe and NATO markets, capturing European defense procurement growth.

Ecosystem Shared Infrastructure — Compressing Marginal Costs

Every company acquired or invested in gains immediate access to the Ondas group's shared infrastructure:

- Manufacturing capacity: Pre-arranged production slots at Tier-1 electronics contract manufacturers (Kitron, Flextronics), dramatically compressing time-to-volume-production.

- Sales channels: Group-wide government and defense client relationships, allowing newly acquired companies to skip years of relationship-building.

This "ecosystem multiplier" architecture means each Ondas Capital investment is not isolated — it is an acceleration node within a compounding system, generating visible scale economies across the portfolio.

III. Financial Perspective: Dilution vs. Asymmetric Returns

Any honest analysis must confront the question investors most worry about: share dilution.

To fund the $1B war chest, Ondas issued substantial stock and warrants, diluting existing shareholders. However, the correct analytical framework is not "how many shares were issued" but rather "what was obtained in exchange."

| Cost | Potential Return |

|---|---|

| Share dilution (already occurred) | Technology asset valuation multiple expansion |

| Near-term EBITDA loss expansion | Elimination of bankruptcy risk + predatory acquisition opportunity window |

| Financing cost (rate/discount) | Distressed acquisition of competitors' assets when capital-constrained rivals can't compete |

More importantly, an early signal has emerged: by early 2025, Ondas Capital's investments in listed companies had generated approximately 85% unrealized gains — preliminary evidence that the team's deal selection and structuring is working as designed.

If Ondas delivers on its multi-hundred-million revenue guidance in 2026, the dilution experienced to date will be judged in hindsight as the necessary price of acquiring a lasting structural advantage — much as Amazon's years of capital consumption were eventually vindicated by its infrastructure dominance.

IV. The Investment Logic Chain — Ondas Capital's Five Strategic Elements

For investors with a long-term orientation, here is the complete analytical framework:

| Strategic Element | Core Asset | Expected Profit Source |

|---|---|---|

| Technology Bridge | Battlefield-proven Eastern European / Israeli technology | U.S. market valuation premium (compliance value-add) |

| NDAA Compliance Advantage | "Made in USA" certification with Chinese components removed | Federal procurement market share after Blue UAS List entry |

| Ecosystem Integration | Shared manufacturing, sales channels, technology IP | Declining marginal costs + cross-sell revenue |

| Portfolio Unrealized Gains | Equity in listed / unlisted acquired companies | Future liquidity events (IPO / acquisition) providing realized returns |

| TRL 7+ Quality Gate | Only invest in operationally validated technologies | Reduced technology risk; compressed time-to-commercialization |

V. Ondas + Palantir: Hardware Meets Software Intelligence

One of the most under-appreciated strategic developments is the emerging Palantir partnership. If Palantir is the AI decision-making brain of modern defense operations — processing sensor data and presenting commanders with decision-ready intelligence — then Ondas is building the physical execution muscle: the drones, ground robots, and stratospheric platforms that actually carry out those decisions.

Neither can fulfill the other's function. Together, they form a complete autonomous operational loop: perceive → decide → execute. The commercial implication: Ondas gains a halo of Palantir's institutional credibility in DoD circles, making combined sales conversations dramatically more compelling than either company could achieve independently.

"Flow follows profit. In today's geopolitical environment, defense budget flow is irreversibly moving toward autonomous systems and counter-drone technology. Ondas Capital is not just the group's finance arm — it is the group's strategic heart."

VI. Risks That Cannot Be Dismissed

✅ Bull Case — The Long-Term Payoff Scenario

- Technology Bridge arbitrage compounds: Each new acquisition raises the platform's combined valuation, attracting more deal flow at more attractive terms — a self-reinforcing advantage cycle.

- Blue UAS List dominance: With competitors locked out by NDAA and DJI effectively banned, Ondas's listed status becomes a sustained near-monopoly in U.S. federal UAS procurement.

- Ecosystem network effects: Shared infrastructure costs decline per unit as each new acquisition joins the platform, improving returns on all prior investments.

- Portfolio liquidity events: Unrealized gains crystallize through IPOs or secondary sales, providing non-dilutive capital recycling.

⚠️ Bear Case — The Risks That Could Derail the Thesis

- Integration velocity exceeds management bandwidth: 5+ simultaneous acquisitions from multiple geographies is an extraordinary execution challenge at any company, let alone a $300M market-cap emerging platform.

- Policy risk: A shift in U.S. defense procurement priorities (e.g., budget sequestration, change in C-UAS doctrine) could alter the timing and volume of expected federal contract flows.

- Dilution acceleration: If capital requirements from additional acquisitions exceed organic cash generation, the pace of share issuance may compress per-share returns even if the enterprise value grows.

- Technology integration complexity: Each acquired company brings different technical architectures. True ecosystem synergies (vs. portfolio-in-name-only) require deeper engineering integration that takes time and skilled management.

📋 Tracking Log

| Date | Event | Judgment | Thesis Change |

|---|---|---|---|

| 2026/01/26 | Initial research published (capital strategy thesis) | ⏸️ Active Watch | Tech Bridge logic confirmed; M&A pipeline under observation |

| 2026/05/17 | Post-Q1 2026 earnings update | ⏸️ Active Watch (upgraded) | Five acquisitions completed; Mistral IDIQ confirmed; thesis materializing |

Next planned update: Post-Q2 2026 earnings (est. August 2026)

Early update triggers: Major new acquisition or divestiture / IDIQ contract award milestones / Blue UAS List additions

Frequently Asked Questions

15+ years in U.S. equities and options strategy. Exchange professional background with direct financial analysis experience. Applies the Four-Filter Defense Screen to evaluate stocks, with a focus on Physical AI, autonomous systems, and defense-tech investment cycles. All analysis based on public SEC filings, company press releases, earnings transcripts, and first-hand industry sources. Not investment advice.

Investing involves risk; please assess your own financial situation carefully before making any decisions.

Data sources: Ondas Inc. SEC Filings, Company Press Releases, Q1 2026 Earnings Call Transcript, Public Records (as of May 2026)

Comments ()