Weekly Market Pulse: Summit Rally Fades, Power Infrastructure Leads for Second Straight Week

Summit produced thinner results than markets priced in. Bond market disappointed. 605 scanned, 89 passed six rigorous criteria. Power infrastructure led for a second week; cybersecurity / SaaS rebound emerging as a potential third theme.

I. Market Action & Sentiment

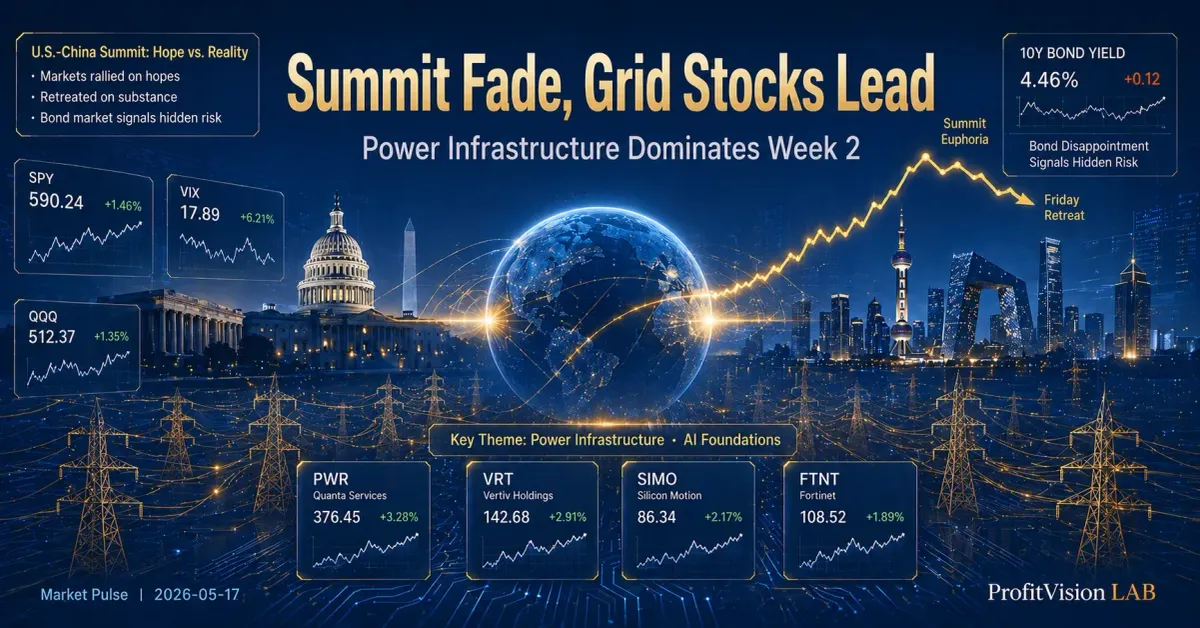

This week's market narrative can be summarized in a single phrase: "Wednesday was the peak; Friday was the reality check." Early in the week, investors entered with elevated expectations for the Trump-Xi summit. Tech stocks were chased higher, and QQQ touched an intraday all-time high of $719.79 on Thursday (May 14). SPY closed at $748.17 on the same day — a near-term sentiment peak for this bull run.

Then Friday (May 15) delivered a dose of geopolitical reality. The summit produced results, just thinner ones than the market had priced in. The US and China agreed to reduce tariffs on roughly $30 billion in "low-to-mid-end consumer goods," in exchange for China purchasing US agricultural products, Boeing aircraft, and crude oil. The biggest tech headline was Nvidia gaining approval to sell H200 chips to Chinese enterprises. However, structural trade barriers, the technology export control framework, and the Taiwan Strait divide — where Xi Jinping explicitly warned that "mishandling the Taiwan issue will threaten the entire US-China relationship" — all saw zero concrete progress. The bond market's reaction was especially blunt: the 30-year Treasury yield barely moved. Treasury Secretary Bessent's goal of pushing long-term rates lower remains far from realized. The S&P 500 fell 1.24% on Friday alone; the VIX jumped from 17.19 to 18.43.

Despite the reversal, the bull market structure remains intact. SPY closed the week at $739.17 (+0.21%), logging a seventh consecutive positive week. The VIX, though ticking higher, remains in the calm zone well below the 25 warning threshold. Core assessment: confirmed bull market, but this week added one distribution day. The "frictionless uptrend" phase has ended — we are entering a stock-picker's market where structural quality matters more than index momentum.

II. Breadth Signals

This week's systematic screen covered over 600 US equities across six research watchlists, applying six rigorous criteria — momentum score, fundamental score, relative strength, institutional flow rating, earnings quality, and industry group rank. The results:

89 stocks passing all six criteria might seem high, but there's a structural explanation: this week's watchlist composition included a larger share of the Near All-Time-High list (209 stocks), which naturally carries a higher pass rate — because stocks still near their highs after a broad correction are themselves survivors of dual momentum-and-fundamental filtering. The more meaningful signal lies elsewhere.

Near Pivot at zero for a second consecutive week is the signal most worth thinking about. Two interpretations are both valid: the constructive view — prior breakout stocks are consolidating gains, waiting for the next wave of institutional buying volume, healthy digestion; the cautious view — if week three also prints zero, it suggests the market's overall offensive intent is declining, and a stock-picker's market is replacing a broad advance. With 54 stocks still passing on the Near All-Time-High list, leading stocks are not yet meaningfully distributing. The bull market skeleton remains structurally intact.

III. Week-Over-Week Rotation

The most notable rotation signal this week was the subtle emergence of a new leadership theme. Cybersecurity and enterprise cloud software names Fortinet (FTNT) and Palo Alto Networks (PANW) both entered the passing list, and both are trading near all-time highs. This has been a rare occurrence in the screen results throughout 2026.

Context matters: in early 2026, market sentiment around "AI will replace enterprise SaaS" was deeply pessimistic. Cloud software valuations were severely compressed, with some names down more than 40% from their peaks. But this week, Wall Street began walking back that narrative — "the expectation that AI will eliminate the entire software industry was massively overstated" — and earnings from companies like Palo Alto Networks showing AI-driven security demand actually expanding prompted tentative capital rotation back into the space. This doesn't confirm a full SaaS recovery. But the directional shift is worth watching.

Another new entrant was DT Midstream (DTM), breaking out of the first stage of a cup base pattern — the week's only valid recent breakout. Its industry classification is oil and gas pipelines, separate from the core power infrastructure theme, suggesting some energy infrastructure capital is moving independently.

The power infrastructure theme maintained its strength overall, though first-tier names (STRL, NVT, DY) showed slightly fewer watchlist appearances than last week — not a sign of fading momentum, but more likely healthy rotation at elevated prices. PWR dominated with four watchlist co-appearances, the most concentrated institutional conviction of any name this week.

IV. Industry Themes

Theme 1: Power Infrastructure (10 stocks passing, dominant position unchanged)

Quanta Services (PWR), Sterling Infrastructure (STRL), nVent Electric (NVT), Dycom Industries (DY), and IES Holdings (IESC) lead, concentrated in heavy construction and electrical equipment sub-industries. The investment logic has been validated repeatedly over the past two weeks: AI data center power demand is growing far faster than grid expansion capacity. The US is installing less than half the high-voltage transmission line capacity actually needed each year, and the licensed electrician shortage is projected to persist at least through 2030. This is not a short-term trade — it is a capex cycle that can be verified quarter by quarter in actual earnings. Notably, after the US-China summit, China agreed to purchase more US energy exports. If that commitment is executed, it provides an additional marginal positive for US LNG export infrastructure and pipeline companies.

Theme 2: AI Semiconductor Full Chain (multiple names, second consecutive week)

Silicon Motion (SIMO), MACOM Technology (MTSI), Analog Devices (ADI), Taiwan Semiconductor ADR (TSM), and Vertiv (VRT) continued to hold their positions in the passing list with multiple watchlist co-appearances. The new catalyst this week came from the summit: Nvidia's H200 chips gaining approval for Chinese enterprise sales creates positive forward signals for NAND flash memory controllers (SIMO), optical networking chips (MTSI), and data center power management (VRT). If China's AI infrastructure buildout accelerates, demand visibility across the entire semiconductor supply chain improves in parallel.

Theme 3: Cybersecurity / SaaS Rebound (emerging, not yet confirmed)

Fortinet (FTNT) and Palo Alto Networks (PANW) entered the screen together — both are world-class next-generation firewall and zero-trust architecture providers. Cybersecurity's unique characteristic is that it is one of the few software sub-sectors where AI-era demand is actually expanding: the proliferation of AI tools is rapidly enlarging enterprise attack surfaces, and security spending is one of the last categories corporate IT budgets are willing to cut. If both names hold their current levels through next week on healthy volume, it will serve as an early confirmation signal for a broader SaaS recovery cycle. The unifying narrative across all three themes: power, chips, cybersecurity — the infrastructure trinity of the AI era.

V. Stocks Worth Watching Next Week (not investment advice)

Before discussing individual names, a note on ProfitVision LAB's three proprietary rating dimensions: PV Institutional Buying Intensity measures capital flow positioning (1–99 percentile, higher = greater institutional concentration); PV Relative Strength reflects the stock's 52-week return percentile within the market (measuring price leadership); PV Earnings Quality Score grades revenue growth, net margin, and return on equity from A to E, with A representing the strongest fundamentals. All ratings are preliminary assessments and do not constitute investment advice.

VI. What to Watch Next Week

Signal 1: Will the Near Pivot list restart in week three?

Zero qualifiers for two consecutive weeks. If three or more names appear near technically defined pivot points next week, digestion is over and a new breakout wave is forming. If it stays at zero or shrinks further, consider whether the market is undergoing a deeper momentum restructuring — and increase selectivity accordingly.

Signal 2: Direction of the 30-year Treasury yield.

This is the most underappreciated risk variable of the week. The US-China summit gave foreign investors no new reason to return to US Treasuries. If long rates remain stubbornly elevated over the next two weeks, high-multiple AI infrastructure names (particularly VRT and PWR) may face valuation multiple compression. Watch for signs of institutional systematic reduction in growth stock exposure.

Signal 3: Can FTNT and PANW hold their highs and confirm cybersecurity as the third theme?

If both names hold their current levels next week on healthy volume, the cybersecurity / SaaS recovery thesis gains significant probability — creating a third fundamentally supported capital theme alongside power infrastructure and AI semiconductors. If they quickly retreat, treat it as tentative dip-buying rather than a trend change.

The core insight this week: the short-term tailwinds from the US-China summit were given back on Friday, but the structural demand logic for power infrastructure and AI semiconductors did not change as a result. The initial cybersecurity warming signal is worth adding to the watchlist. Until the bond market clarifies its direction, selecting stocks with strong structural setups is preferable to chasing index momentum.

This Week's ProfitVision LAB Featured Articles

This article is produced by ProfitVision LAB. All content is based on publicly available market data and systematic screening results, for educational and informational purposes only. Nothing herein constitutes a buy, sell, or hold recommendation for any individual security, nor does it constitute any form of investment advisory service or financial advice. Investing involves risk; past performance does not guarantee future results. Any securities mentioned are analytical examples only and do not represent the actual holdings of ProfitVision LAB or Shiba the Disciplined. Readers should make independent judgments based on their own financial situation, risk tolerance, and investment objectives, and consult a qualified investment advisor when appropriate.

Comments ()