When Risk Appetite Reverses: Why I Permanently Excluded ARK-Type Narrative Assets

Some losses erode more than capital — they erode judgment and discipline. My 2020–22 ARK losses became the catalyst for a probability-based options-seller system. The Narrative Asset Filter permanently excludes assets that are valuation-opaque, cash-flow-free, and narrative-dependent.

ProfitVision LAB | Trading Psychology · Asset Allocation Philosophy | May 2026 | 10 min read

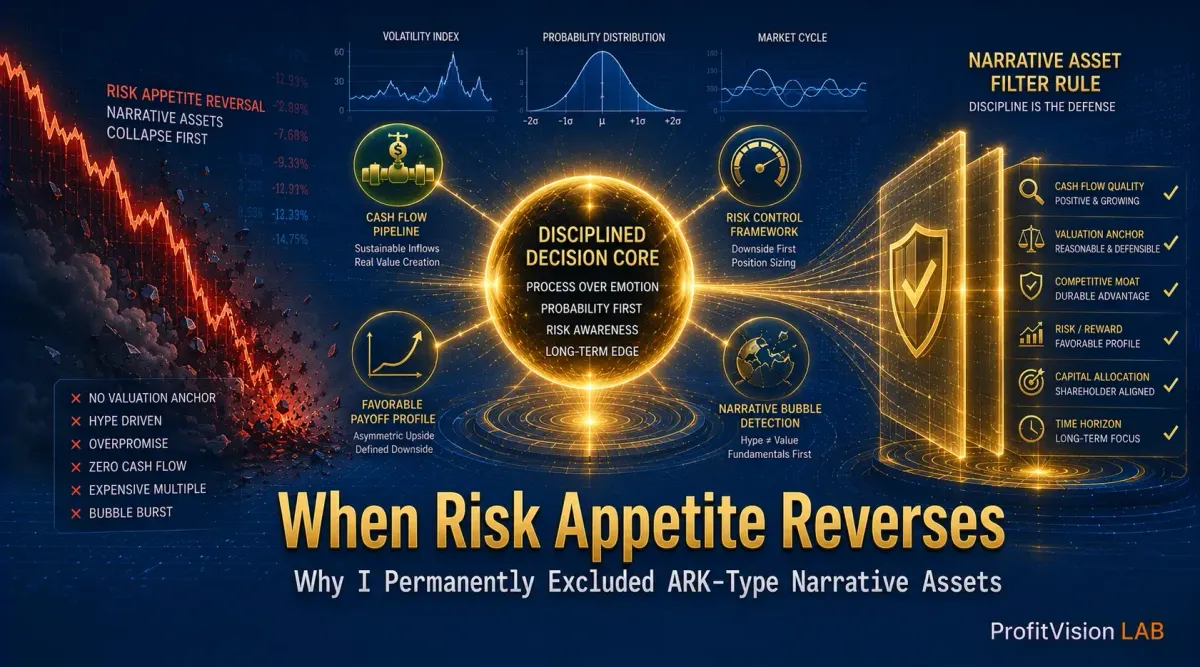

- ARK-type narrative assets have no valuation anchor — their valuation logic rests entirely on whether the market continues to believe the story. When risk appetite reverses, they are the first to be liquidated.

- Cash flow is not just a return mechanism — it is a decision stabilizer. Holding assets without cash flow chronically erodes judgment quality during drawdowns, which is more dangerous than the paper loss itself.

- The Narrative Asset Filter — three simultaneous conditions: valuation-opaque, no stable cash flow, returns dependent on future narratives. Any asset meeting all three is permanently excluded from the core portfolio.

- Mature investing is not about forcing yourself to adapt to every asset class. It is about clearly identifying which assets are incompatible with your personality structure — self-knowledge is a competitive edge.

- The greatest risk in an investment system is not volatility — it is losing discipline. Non-negotiable filter rules are the foundation of long-term system survival.

Some investment losses eventually become tuition. Others do not just cost money — they slowly erode your judgment, your discipline, and your entire decision-making architecture.

For me, ARK belongs to the second category.

I am formally placing the entire ARK ETF lineup (ARKK / ARKW / ARKF / ARKG / ARKQ / ARKX) on my Do Not Touch List — permanently.

This is not a sudden bearish call on technological innovation, nor a verdict on Cathie Wood. I fully understand ARK's worldview. AI, gene editing, autonomous vehicles, robotics, fintech — these technologies may profoundly reshape the world over the next decade. I believe in the direction.

The real question is: When market Risk Appetite begins to reverse, what happens to these assets?

My answer: they tend to become the market's highest-priority liquidation targets.

Why "Thinking You Understand It" Is the Most Dangerous Trap

Most people attribute investment failure to ignorance. But the most dangerous thing about ARK was precisely the opposite: I thought I understood it perfectly.

I had researched its holdings, grasped the disruptive innovation narrative, and knew it was betting on the next decade of technological transformation. I genuinely believed I was "positioning ahead of the future" — and that truly great opportunities were never supposed to feel comfortable.

What followed was: severe drawdowns, prolonged dead weight, emotions held hostage by price action.

The truly frightening part was not the loss itself — it was that my decision-making quality began to deteriorate. I checked prices more frequently, tracked news daily, sought out voices online that confirmed my thesis, and started rationalizing risk with "just wait, it'll come back."

In the end, I had to admit: I did not lose to the market. I lost to the wrong asset classification.

Why Do ARK-Type Assets Lack a Valuation Anchor?

The core issue: ARK's valuation logic is not built on stable free cash flow, a proven business model, or shareholder returns. It rests on a far more fragile foundation — whether the market is willing to keep believing the future story.

Many of these companies operate at persistent losses, yet command extreme valuations because the market assigns a "dream premium." Structurally, they rely on high P/S multiples rather than present-day earnings power. In environments of abundant liquidity and elevated risk appetite, these assets surge the hardest — because the market is willing to ignore profitability, ignore valuation, ignore cash flow, and chase "future potential" alone.

The problem: once risk appetite shifts, the entire valuation logic inverts instantly. When the Fed tightens, liquidity contracts, and capital seeks certainty — the market stops paying for "dreams a decade away." The assets abandoned first are precisely those with no cash flow buffer, sustained only by narrative. There is no valuation anchor to find a floor. There is no way to know when the market will stop compressing multiples. Once capital flows reverse, these names fall hardest, correct deepest, and take far longer to recover than most investors can psychologically withstand.

My real mistake was not buying ARK. It was confusing "narrative stability" with "risk controllability."

What Is Cash Flow's True Function?

Cash flow is not just a return mechanism — it is a decision stabilizer. When you hold an asset that continuously generates cash flow, even if the price falls short-term, you still receive a positive signal: dividends, options premium, growing Free Cash Flow (FCF), or buybacks. These signals remind you: the asset is still operating; the business logic is still intact.

ARK is the second column. Its return source depends entirely on future valuation expansion. If the market stops assigning a higher dream multiple, holders receive nothing. They simply wait.

Some Assets Are Incompatible With Your Personality Structure

The deepest insight from this experience was finally admitting something I had avoided: certain assets are structurally incompatible with certain personalities.

ARK's investment language is engineered to activate a specific psychological mode:

These narratives systematically triggered my most dangerous behavioral patterns: oversizing, holding through signals, averaging down, delaying the Loss-Exit, and using future hope to justify present risk overflow.

This was not a technical problem. It was a personality compatibility problem. Some investors are naturally suited to high-volatility narrative assets. I am not. Mature investing is not about forcing yourself to become someone else — it is about clearly understanding what you are not suited for. Self-knowledge is a competitive advantage.

DXYZ Confirmed It: My Pattern Recognition Is Evolving

The recently popular DXYZ is structurally similar — private unicorn exposure, pre-IPO narrative, imagination-driven valuation premium, highly subjective pricing. The story is compelling.

But this time, before placing any order, I felt instinctively uncomfortable and ultimately walked away.

Not because I had become conservative. But because I could now recognize the pattern: any asset simultaneously exhibiting opaque valuation, absent stable cash flow, and returns contingent on future events — that is not an investment for me. That is a Mentally Draining Asset. ARK and DXYZ have different structures, but the psychological outcome they produce in me is the same category of thing.

What Is a "Mentally Draining Asset" — and How Do You Filter Them Out?

ProfitVision Narrative Asset Filter Rule

Starting today, I am establishing a non-negotiable rule for myself:

Any position that simultaneously meets all three of the following conditions —

- Valuation is opaque or highly subjective

- No stable cash flow

- Investment thesis is highly dependent on future events or narratives

- Prohibited from entering the core portfolio

- Prohibited from becoming a concentrated position

- Prohibited from influencing the long-term cash flow system

For the systematic stock selection framework behind this rule, see the 【ProfitVision Four-Layer Defensive Screen】.

Why Return Rate Is Not the Most Important Metric in Investing

The genuinely difficult challenge is not generating large returns — it is building a system you can execute consistently for ten, twenty, or even fifty years.

What ARK taught me was not which ETF is good or bad. It was something more fundamental:

Any asset that disrupts my sleep, compels me to check prices obsessively, triggers emotional volatility, or erodes operational discipline — regardless of its future upside potential — is the wrong asset for me.

For me, permanently excluding ARK-type assets is not a market call. It is a decision about self-knowledge and system protection.

Investors should make their own judgments based on their individual risk tolerance, financial situation, and investment objectives, and bear the corresponding risks.

Comments ()