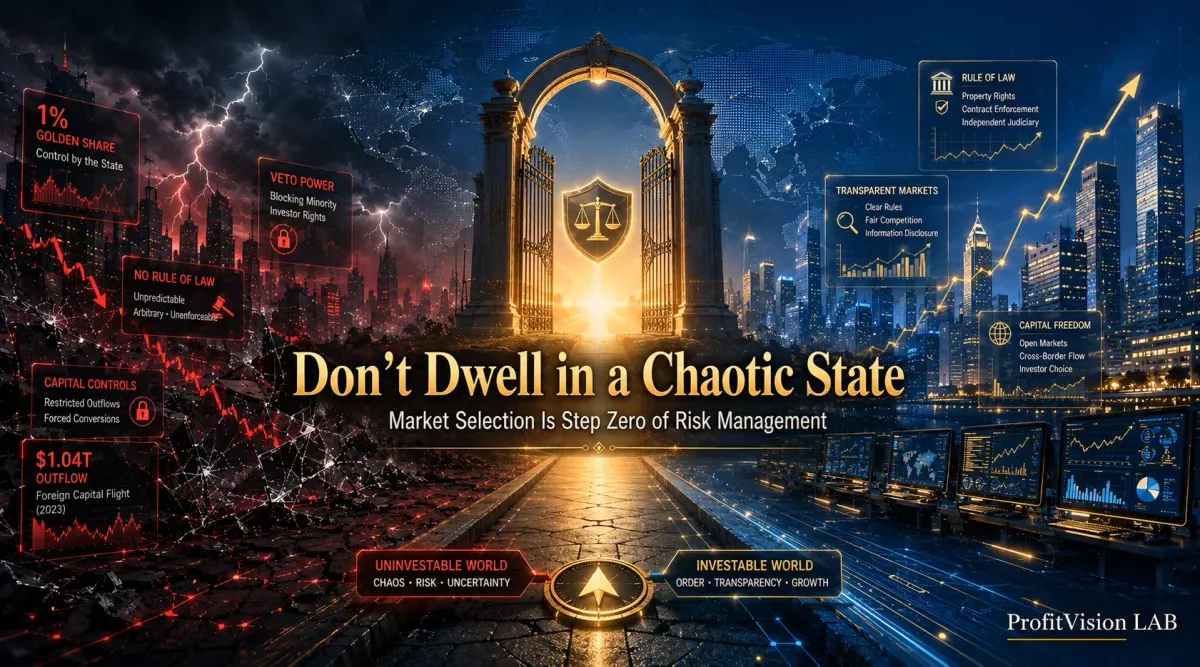

Don't Dwell in a Chaotic State: Choosing the Right Market Is Risk Management's First Move

Chinese stock discounts aren't a bargain — they're rational risk pricing. From golden share veto rights to the 2021 crash and 2026 cross-border broker crackdown, Shiba the Disciplined breaks down why market selection is the true first step in risk management.

Most investors think of risk management as stop-losses, position sizing, and hedging tools. But there is a more fundamental question that rarely gets asked: which market you choose to operate in is the true first move in risk management.

📌 Key Thesis

- Chinese stock discounts are not a bargain — they are the market's rational pricing of uninvestability risk

- The Golden Share mechanism: state capital holds 1% but wields veto power over major decisions — these aren't companies, they're state agencies in corporate clothing

- 2021: six regulatory strikes in twelve months, each unpredictable, collectively devastating

- 2026: the cross-border broker crackdown shows even domestic capital flows are being sealed off — smart money has been voting with its feet

- Four standards for assessing market investability: rule predictability, symmetric capital flows, clear political-commercial boundary, and enforceable shareholder protections

This Isn't Cheap — It's a Risk Discount

Chinese equities have long traded at roughly half the valuation of comparable U.S. technology companies. Many investors frame this as opportunity: the market is short-sighted, foreign capital is being emotional, mean reversion is inevitable.

I disagree.

Markets make mistakes, but they rarely make the same mistake for years at a stretch. When a discount persists — and is continually reinforced by new events — the right question isn't "why is this so cheap?" It's: "What risk is the market pricing that I haven't accounted for?"

That unknown has a precise name: policy risk — and it cannot be hedged.

When you buy a U.S.-listed company, you know it is subject to SEC oversight, that shareholder rights are codified in law, and that management's fiduciary duty runs to stockholders. When you buy a Chinese equity, you are accepting an entirely different set of rules — rules that can be rewritten at any time, by any of several regulatory bodies, with no prior notice.

You're Not Buying a Company — You're Buying the Government's Permission to Profit

Here is the structural issue that most investors overlook: the Golden Share (Special Management Share) mechanism.

State capital acquires a small ownership stake — typically 1% — in a company's key domestic entity, paired with special rights that grant a veto over major business decisions. One percent of the equity. One hundred percent of the power to block.

This is not theoretical. It has already been applied to Alibaba, Tencent, and ByteDance — companies that most investors classify as "private technology firms."

Take ByteDance, parent company of TikTok. Corporate registration records show that ByteDance's key mainland entity is 99% owned by Douyin Co., Ltd. and 1% owned by Wangtouzhongwen (Beijing) Technology Co., Ltd. — "NetVenture Zhongwen." That 1% entity is itself owned by three state institutions: the Cyberspace Administration of China's investment fund (co-founded by the CAC and the Ministry of Finance), a subsidiary of China Media Group, and Beijing Cultural Investment Development Group.

One percent ownership. One board seat. And through the Special Management Share structure: one veto over any decision that touches content, data, or "national security."

As a public-market participant holding the other 99% (indirectly), your shareholder rights exist only on the condition that the government chooses not to exercise its veto. The moment policy direction shifts, every fundamental analysis, Economic Moat assessment, and DCF model you built becomes irrelevant.

This is not a company in the conventional sense. It is a commercial extension of state authority. You are not buying equity in a shareholder-first enterprise. You are buying a ticket that says: "You may share in the profits — within whatever boundaries the government defines, for as long as the government permits."

That ticket sometimes pays well. But its value is determined by the government's current policy appetite, not the company's commercial logic.

2021: A Scripted Catastrophe

The 2021 Chinese equity collapse is the best case study for understanding this market. Not because of the magnitude of the drawdown — 85% is brutal by any measure — but because of what it demonstrates: how fast rules can change, and how impossible they are to predict.

2026: They're Not Even Letting Their Own Money Leave

The 2021 story is widely known. What happened in May 2026 shows the logic hasn't ended — it has escalated.

China's CSRC, acting jointly with the People's Bank of China and six other government agencies, announced enforcement actions against Futu Holdings (FUTU), Tiger Brokers' parent UP Fintech (TIGR), and Longbridge Securities. The charge: illegally providing cross-border securities services to mainland Chinese residents without regulatory authorization.

peak pre-market decline

peak pre-market decline

unprecedented scale

The fine amounts are secondary. The operational consequence is what matters: during a 2-year wind-down period, affected mainland Chinese clients may only sell existing positions and withdraw funds — no new investments permitted. You are allowed to exit. You are not allowed to re-enter.

Behind that signal sits a number: in 2025, Chinese capital outflows reached $1.04 trillion — the largest annual outflow on record since 2006. Smart money had already been voting with its feet. The government's response was to lock the door.

When capital flows are asymmetric — easier to enter than to exit — a rational market demands a "locked-in discount." That discount is exactly what you see reflected in the valuation gap.

What Makes a Market Worth Living In: Four Standards

This is not an argument to never touch Chinese equities, or to treat U.S. markets as risk-free. Every market carries risk. The discipline is in knowing precisely what risk you are taking before you commit capital.

When assessing a market's investability, I apply four dimensions:

| Dimension | Definition | China Assessment |

|---|---|---|

| ① Rule Predictability | Regulatory logic is transparent; changes follow process; the table doesn't get flipped overnight | High Risk Policy can reverse without notice across any sector |

| ② Symmetric Capital Flows | Capital enters and exits on equal terms; profits can be repatriated; no one-way valves | High Risk Capital account controls restrict cross-border movement |

| ③ Clear Political-Commercial Boundary | Government is referee, not player — and definitely not team owner | High Risk Golden Share mechanism makes state a silent controlling party |

| ④ Enforceable Shareholder Rights | Even minority shareholders have real, actionable legal remedies | High Risk Litigation channels limited; policy consistently overrides shareholder interest |

Four dimensions, four high-risk ratings. This doesn't mean Chinese assets never appreciate, or that there are no tactical trading opportunities. It means any long-term, fundamentals-based holding thesis carries a structural discount that must be explicitly acknowledged and priced in.

That discount is what you're looking at when you see the "cheap" valuation on your screen.

Don't Dwell in a Chaotic State: The Zero-th Step of Risk Management

Confucius wrote: "Do not enter a state in peril; do not dwell in a state in chaos." This wasn't cowardice. It was the recognition that in an environment where the rules can be overturned at any moment, individual judgment and effort cannot overcome systemic uncertainty.

Investing is no different.

In a market where a 1% golden share can veto your entire fundamental analysis, your DCF model, Economic Moat assessment, and technical setup are all built on sand. In a market where a government can eliminate an entire industry overnight, your sector research can become worthless before morning. In a market where even citizens' own capital is blocked from leaving freely, foreign investors' valuation discounts are rational — not emotional.

Most investors begin risk management by setting a stop-loss. True risk management begins with choosing the market.

Choosing the right market is the true first step in risk management.

Or more precisely: it is Step Zero.

Comments ()