AI 算力大戰進入 ROI 檢驗期:六道結構性檢驗下的投資地圖 2026 Q1 財報季結束,市場開始用更高的標準篩選誰真的能變現。本文以六道結構性檢驗繪製 AI 算力大戰進入 ROI 檢驗期後的投資地圖——從 6,500 億美元 CapEx 的真實風險、不論誰贏都受益的中立瓶頸、SaaS 變現分水嶺、AI 越強資安越呈指數成長的反向邏輯,到 NVIDIA 已布好的五道反擊。

AI Compute Wars Enter the ROI Verification Phase Q1 2026 earnings revealed AI investment has entered the 'promises must materialize' phase. Six structural checkpoints map the landscape: CapEx risks, silicon-agnostic bottlenecks, SaaS watershed, exponential cybersecurity demand, NVIDIA's five-layer counterattack.

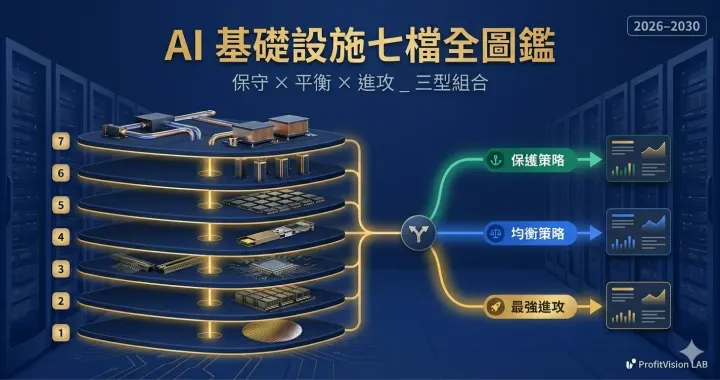

AI 基礎設施七檔長期持股全圖鑑:保守/平衡/進攻三型組合配置(2026–2030) 十年大潮已啟動:超大規模業者 2026 capex 達 $6,600 億美元、AI 加速器 CAGR 54-56%。本研究從七層 AI 工廠堆疊出發,介紹 TSM、NVDA、ALAB、FN、台達電、VRT、奇鋐 七檔候選,並提供保守、平衡、進攻三型配置組合,讓不同風險偏好都能找到適合自己的 AI 基礎設施部位。

TSMC (TSM): Physical Monopolist of the AI Era TSMC is the only physical chokepoint of the AI era — over 90% of advanced AI chips pass through its fabs. Q1 2026: record 66.2% gross margin, HPC at 61% of revenue, $52–56B capex locking in the N2/A16 and CoWoS moat. Geopolitics remains the only tail risk worth respecting.

台積電 (TSM) 深度研究:AI 時代的物理壟斷者,無可替代的代工帝國 Q1 2026 毛利率 66.2%、HPC 佔比 61%、EPS TWD 22.08,台積電以史上最強財報證明 AI 時代的物理壟斷地位。N2 製程量產加速、A16 H2 2026 到來、Capex $52–56B 創歷史新高,三星與英特爾的差距只在擴大。含長線現貨 DCA 策略解析,選擇權投資人待 A/D 升至 B+ 後啟動 Bull Put Spread。