Ondas Holdings (ONDS) Deep Research Part 1: Physical AI Trinity — Neural Network, Autonomous Body & Dual Regulatory Moat

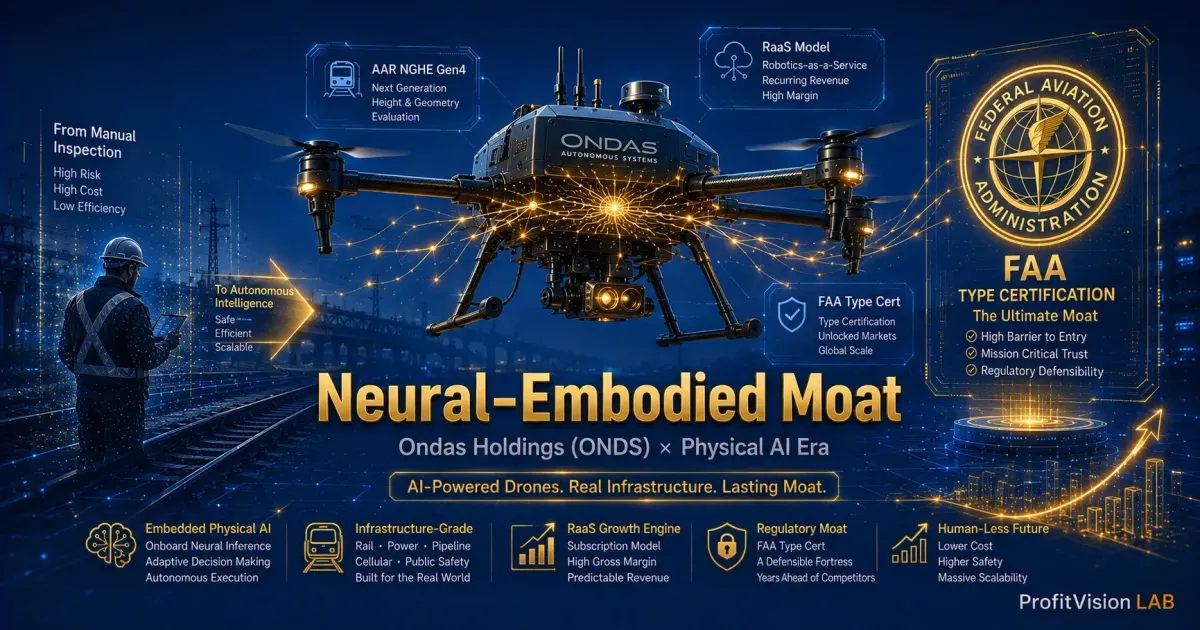

Ondas (ONDS) holds America's first FAA Type Certification for BVLOS autonomous drones and the sole AAR NGHE Gen4 rail comms standard — a dual regulatory moat rivals cannot replicate for years. Q1 2026: revenue +1,065% YoY, gross margin 49%, backlog $457M, cash $1.48B.

IEEE dot16 standard monopoly + America's first FAA Type Certification for BVLOS: The two regulatory moats that make ONDS virtually immune to competition in Physical AI infrastructure.

2026.05.17 | Shiba the Disciplined | ProfitVision LAB | Last Updated: 2026.05.17 | Est. read time: 14 min

🔍 Four-Filter Screening Summary

| Filter | Metric | Data | Result |

|---|---|---|---|

| Filter 1: Institutional Flow | Institutional participation / capital raises | 2025–2026: $1B+ raised; institutional heavy entry | ✅ Clear |

| Filter 2: Economic Moat | FAA Type Cert / AAR NGHE Gen4 standard | First-of-kind Type Cert (no comparable peer); AAR exclusive supply | ✅ Clear |

| Filter 3: Financial Resilience | Gross margin / cash / backlog | GM 49%; Cash $1.48B; Backlog $457M | ⏸ Watch (Adj. EBITDA still negative) |

| Filter 4: Technical Trend | Revenue acceleration / repricing momentum | Q1 2026 YoY +1,065%; FY guide $390M; strong momentum | ✅ Clear |

Chapter 1: Industry Landscape — The Three-Layer Physical AI Stack

Throughout the 2024–2026 AI cycle, most investor attention flocked to NVIDIA's compute infrastructure. But Jensen Huang's repeated emphasis on "Physical AI" is quietly taking shape as the next wave: AI systems migrating from cloud servers into railways, oil fields, defense perimeters, and smart cities. This transition requires three fundamentally distinct infrastructure layers.

The AI brain

Industrial private wireless nervous system

Drone + robotic body

Ondas simultaneously occupies the communication layer and the execution layer — a rare form of vertical integration in the Physical AI ecosystem. The addressable markets are substantial: global industrial wireless communications (~$30B TAM), Drone/Robot-as-a-Service (DaaS/RaaS, projected >$50B by 2030), and global Counter-UAS (C-UAS, >$10B by 2030). Combined, Ondas's total addressable market exceeds $100B.

Physical AI refers to the integration of artificial intelligence into real-world autonomous systems — drones, robots, self-driving vehicles — enabling them to perceive, decide, and act in physical environments rather than purely digital ones. NVIDIA calls it "the next wave of AI," representing AI's expansion from software into industry, defense, and transportation.

For investors, the critical insight is this: Physical AI demands tight vertical integration of communications, hardware, and software. The barriers to entry are far higher than pure-software AI, and the moats are correspondingly deeper and more durable.

Chapter 2: Business Model & Economic Moat — The Compounding Power of Standard Monopoly

2-1 Ondas Networks: Turning a Technical Standard Into a Legal Monopoly

The core of Ondas Networks is the IEEE 802.16s/t (dot16) standard's FullMAX Software-Defined Radio (SDR) platform. Understanding this competitive barrier requires understanding a fundamental challenge in industrial communications.

Industrial operators like railways and utilities own fragmented, non-contiguous narrow-band spectrum. Purchasing full 5G bandwidth is prohibitively expensive. Ondas's FullMAX SDR platform software-defines these "spectrum fragments" into aggregated broadband transmission capacity — essentially stitching together abandoned single-lane dirt roads into a software-defined highway.

Physical isolation is a second key advantage: public 4G/5G is the first infrastructure to fail during disasters or cyber attacks. Ondas's private industrial networks maintain critical command integrity under extreme conditions. For railway brake control or military robotics, this is a life-or-death distinction.

Ondas Networks' Economic Moat has three compounding layers:

| Moat Layer | Specifics | Competitor Barrier to Entry |

|---|---|---|

| Technical Standard | IEEE 802.16s/t — the only global industrial narrow-band aggregation standard | Requires fresh IEEE ratification — 5+ years minimum |

| Regulatory Binding | AAR designated dot16 as the sole communication protocol for NGHE Gen4 | Must win a new AAR competitive selection — near impossible |

| System Embedding | Directly integrated into train safety control loops (brake monitoring) | Replacement cost is prohibitive; customers have zero motivation to switch |

2-2 AAR NGHE Gen4: America's Mandatory Fleet Refresh Mandate

The Association of American Railroads (AAR) formally selected dot16 as the communication standard for the Next Generation Head-of-Train Equipment (NGHE Gen4). From a financial analysis perspective, this is effectively a long-term mandatory procurement authorization: tens of thousands of North American freight car units must install new-standard equipment, creating a predictable, large-scale hardware replacement cycle layered with long-term software licensing revenue.

This "regulation-driven mandatory replacement + recurring service fees" model closely resembles the ARR logic of a SaaS company — but with a customer base that cannot defect without re-entering a multi-year regulatory certification process.

2-3 OAS: The RaaS Three-Layer Revenue Architecture

Ondas Autonomous Systems is building a three-layer progressive revenue model — this is the core driver of its valuation repricing potential:

One-time CapEx revenue

Annual OpEx fees

(Recurring ARR)

AI analytics & insights

(Highest-margin layer)

Customers don't need to purchase robots outright — they pay annual subscription fees, converting capital expenditure to operating expenditure and dramatically lowering procurement barriers. As Optimus robots automatically scan facilities daily and generate 3D models and AI analytics, the data layer's stickiness far exceeds the hardware itself — the essence of the RaaS model, and the reason competitors struggle to replicate it.

Chapter 3: Competitive Dynamics — Who Is the Real Threat?

Ondas faces fundamentally different competitive landscapes across its two business lines. In communications (Networks), the threat comes from public 5G penetration. In autonomous systems (OAS), the threats come from Chinese manufacturers and large U.S. defense primes.

| Competitor | Overlap | Strengths | Weaknesses |

|---|---|---|---|

| DJI | Industrial drones | Ultra-low cost; global market share leader | Banned from U.S. federal procurement under NDAA; no FAA Type Cert |

| Skydio | Industrial / military drones | Leading AI autonomous flight | No FAA Type Cert; lacks C-UAS and ground integration breadth |

| L3Harris / RTX | Defense electronics / C-UAS | Strong government relationships; capital-rich | Large but slow-moving; lacks Ondas's vertical integration ecosystem |

| Palantir (partner, not competitor) | AI decision platform | Deep DoD relationships | No hardware execution capability — Ondas's complementary space |

| Verizon / AT&T (5G) | Industrial wireless | Strong brand; wide coverage | Public networks cannot meet industrial physical isolation requirements; don't meet AAR standard |

Who is the real threat? In the near term, the most significant risk is not competitive displacement — it is execution risk: can Ondas maintain integration quality during rapid expansion, and will regulatory certification timelines stay on track? DJI is effectively excluded from U.S. government markets by NDAA policy. Skydio lacks system integration breadth. Traditional large defense primes move at a pace far too slow to catch Ondas in its early-mover window.

Chapter 4: Financial Resilience — Is the Cash Runway Long Enough?

ONDS posted Q1 2026 GAAP net income of $361M, yet Adjusted EBITDA was still -$10.88M loss. The gap comes primarily from non-cash items: warrant fair value changes (+$390M, non-cash) and subsidiary deconsolidation gains (+$51.5M, non-cash). These numbers look impressive on the income statement, but not a single dollar hit the bank account.

⚠️ For early-stage growth companies, investors should prioritize Adjusted EBITDA (operating P&L after stripping non-cash and one-time items) rather than being misled by headline GAAP figures. The real question: when will cash operating breakeven arrive?

| Metric | Q1 2025 | Q4 2025 | Q1 2026 | Trend |

|---|---|---|---|---|

| Revenue | $4.25M | $30.1M | $50.1M | 🟢 Accelerating |

| Gross Margin | 35% | 42% | 49% | 🟢 Expanding |

| Adj. EBITDA | -$7.49M | — | -$10.88M | 🟡 Loss slightly wider |

| Cash + Short-term Investments | — | ~$616M | $1.48B | 🟢 Sharply increased |

| Pro Forma Backlog | — | $68.3M | $457M | 🟢 Explosive growth |

Is the cash enough? With $1.48 billion in cash, at current burn rates Ondas has ample runway for several years even without new revenue. This definitively eliminates near-term liquidity concerns — which is precisely the strategic intent of the 2025 capital raise. The gross margin expansion from 35% to 49% is particularly significant: it reflects product mix shifting toward higher-margin C-UAS systems and fixed-cost operating leverage. If H2 2026 revenues accelerate as guided, gross margins could breach 50%.

Chapter 5: Valuation & Scenario Analysis — Which Scenario Are You Buying Into?

Given that Ondas has not yet achieved company-level EBITDA breakeven, traditional P/E valuation does not apply. We use EV/Revenue multiples and scenario assumptions — without forecasting a price target.

| Scenario | FY2026 Revenue | Gross Margin | EBITDA Path | Investment Implication |

|---|---|---|---|---|

| 🟢 Bull | $450M+ (beats guidance) | 52%+ | Q4 2026 early breakeven | Market applies SaaS-like high-multiple; significant re-rating |

| 🟡 Base | $390–420M (in-line with guidance) | 49–51% | Q1 2027 (on schedule) | Thesis progressively validated; valuation gradually re-rates |

| 🔴 Bear | Below $350M (misses guidance) | Below 45% | Pushed to 2028+ | Acquisition integration failures; market confidence shaken; meaningful drawdown |

Current market pricing appears to be between the base and bull scenarios, reflecting investors' positive interpretation of Q1 results but retaining a discount for execution risk. If Q2 2026 Adjusted EBITDA loss confirms a "peak" as management projected and converges meaningfully in H2, the probability of the bull scenario increases substantially.

Chapter 6: Investment Thesis & Tactical Outlook

Core Thesis: Ondas is the deepest "regulatory-moat" investment in the Physical AI era. The FAA Type Certification and AAR NGHE Gen4 standard — two "regulatory licenses" — are virtually irreplicable across the peer universe and form the foundation for long-term excess returns.

✅ Bull Case — Why It Deserves a Long-Term Core Position

- Dual regulatory moat is irreplicable: FAA Type Certification (first-of-kind) + AAR NGHE Gen4 sole standard. Competitors need 3–5+ years just to have a path to parity.

- Backlog provides extraordinary visibility: $457M pro forma backlog equals roughly 1.17× the full-year guidance, far exceeding what a typical early-stage growth company can offer.

- RaaS transition unlocks compounding ARR: Each incremental industrial customer added is not a one-time revenue event but a long-term repeatable cash flow — the SaaS-ification of the business model is now established.

- Ample capital war chest: $1.48B cash enables opportunistic M&A acquisitions at distressed valuations when competitors run out of capital.

⚠️ Bear Case — Risks You Must Acknowledge

- Execution risk from rapid M&A: Completing 5+ acquisitions in a single quarter, each from different countries and cultures, demands management bandwidth that has not yet been proven at scale.

- Ongoing dilution pressure: A large overhang of unexercised warrants means future share count growth cannot be ignored; EPS path may compress.

- EBITDA breakeven delay risk: If Q2 loss does not peak or H2 revenue acceleration disappoints, market sentiment can reverse sharply.

- Geopolitical and procurement policy exposure: Significant reliance on U.S., Middle East, and European defense budgets; policy changes can affect procurement decision timelines.

"Flow follows profit. In the defense-tech world, flow is government procurement budgets — and Ondas holds the regulatory entry tickets that make those budgets required to flow through it."

Tactically, ONDS is suited as a long-term core position, not a short-term trading vehicle. Two key monitoring triggers: ① Does Q2 2026 Adjusted EBITDA confirm a peak? ② Does Q3 2026 revenue deliver the expected H2 acceleration? Any significant deviation from either warrants a position reassessment.

📋 Tracking Log

| Date | Event | Judgment | Thesis Change |

|---|---|---|---|

| 2026/01/26 | Initial research published (three-part series) | ⏸️ Active Watch | Regulatory moat confirmed; capital strategy clearly laid out |

| 2026/05/17 | Post-Q1 2026 earnings update | ⏸️ Active Watch (upgraded) | Thesis broadly validated; core risk shifts to integration execution |

Next planned update: Post-Q2 2026 earnings (est. August 2026)

Early update triggers: Major new acquisition announced / EBITDA materially deviates from guidance / key contract cancellation or delay

Frequently Asked Questions

15+ years in U.S. equities and options strategy. Applies the Four-Filter Defense Screen to systematically evaluate individual stocks and reduce emotional noise in investment decisions. Tracks Physical AI, autonomous systems, and defense-tech markets through primary research. All analysis is based on public SEC filings, earnings transcripts, and first-hand industry sources. Not investment advice.

Investing involves risk; please assess your own financial situation carefully before making any decisions.

Data sources: Ondas Inc. SEC Filings, Q1 2026 Earnings Call Transcript, Company Press Releases (as of May 2026)

Comments ()