Danaher / DBS: We Buy You, Then Make You Better — System-Embedded M&A and the Boundaries of Trust

DBS is not just a management toolkit — it is Danaher's M&A architecture for building trust through transformation. Vision, ambition, execution, tolerance, and localization: the real challenges for companies aspiring to grow through M&A.

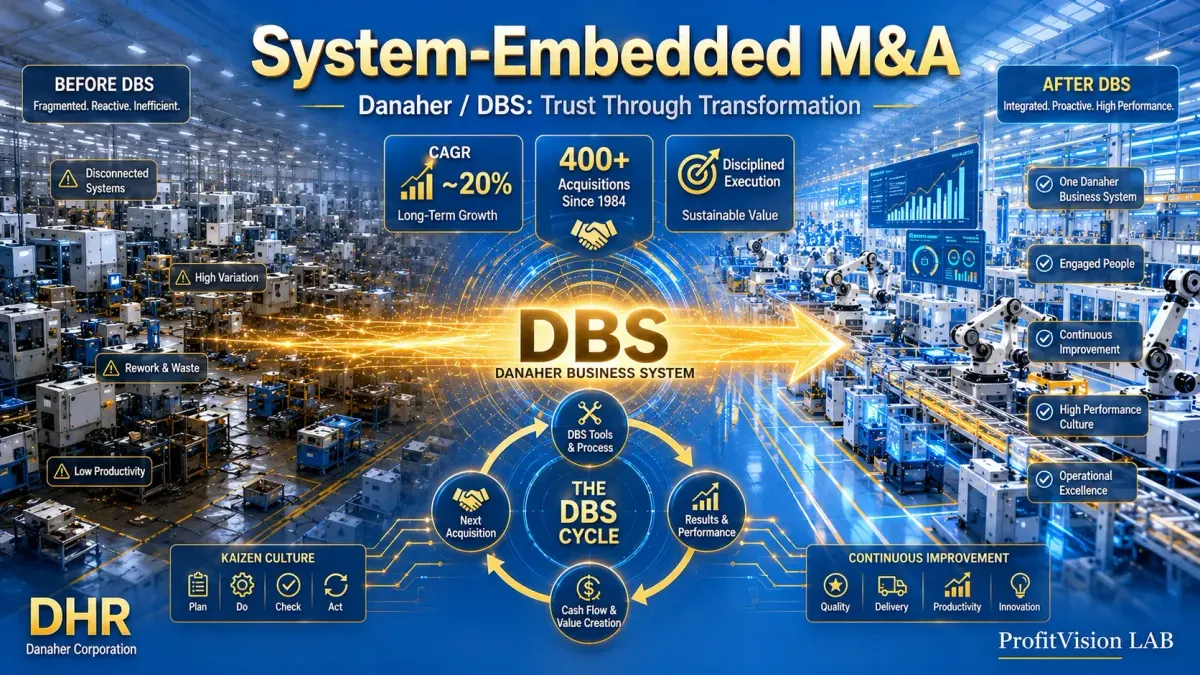

- DBS (Danaher Business System) is not a management consulting tool — it is Danaher's core competitive advantage. It makes acquired companies stronger after integration, and that itself is how trust is built.

- The trust logic of system-embedded M&A is the direct inverse of CSU: Constellation wins trust by "never changing" what it acquires; Danaher wins trust by delivering transformation results.

- DBS functions as a powerful acquisition filter: only businesses with genuine "continuous improvement potential" are worth buying. This is why Danaher's deal success rate far exceeds the average strategic acquirer.

- The Taiwan insight: Taiwanese companies lack neither systems, capital, nor execution capability — what they lack is the vision and ambition to imagine what M&A can make them become, and the tolerance to let acquired companies truly take root locally.

What happens on Day One after Danaher buys you?

Something does happen — the DBS team walks in the door. That is where Danaher diverges from Constellation Software from the very first morning.

Imagine you are the founder of an industrial measurement instruments company. You have just sold your business to Danaher. You assumed that once the deal closed, you could walk away with your proceeds. But on day three after closing, a team of Danaher DBS (Danaher Business System) specialists arrives at your factory. They are not there to conduct an audit. They are not there to cut headcount. They are carrying stopwatches and sticky notes, observing your production line.

The questions they ask seem strange: "How many steps does this component take to travel from the warehouse to the assembly line?" "What is the standard cycle time for this operation?" "Where do you store your customer complaint records?"

Three months later, your production efficiency has improved by 23%. On-time delivery has risen from 71% to 94%. Your cash conversion cycle has shortened by 18 days. Your plant manager says: "This is the most effective operational transformation I have ever seen."

That is how DBS enters. Not a promise of "we will never touch you" — but a promise of "we will make you better," followed by actually delivering it.

Where did DBS come from? Danaher's origin and evolution

The Danaher story begins in 1984 with an obscure real estate investment trust. Brothers Steven Rales and Mitchell Rales acquired the company and began transforming it into an industrial conglomerate — originally called Diversified Mortgage Investors, renamed Danaher in 1985 after a fly-fishing river in Montana.

What changed everything was the Rales brothers' discovery of the Toyota Production System (TPS) in the late 1980s. They did not simply read a few books. They systematically rewrote Toyota's Kaizen (continuous improvement) philosophy into an acquisition integration toolkit — this became the prototype of DBS.

From 2001 to 2014, under CEO Larry Culp, DBS evolved from a manufacturing improvement tool into a company-wide operating system spanning sales, marketing, R&D, and talent development. Culp was later appointed CEO of General Electric in 2018, tasked with applying the same philosophy to rescue a crumbling industrial empire — a fact that speaks to how highly markets regard DBS as a genuine management capability.

(1984–2024)

(1986–2014)

(cumulative, across companies)

What exactly is DBS? Four components, one transformation logic

DBS is not a software system. It is not a consulting report. It is an organic body composed of tools, culture, and people. Its core logic is: find waste, then eliminate it — forever, and never be satisfied with the status quo.

These four components form a self-reinforcing flywheel:

Danaher's moat has three layers. Layer one is the DBS toolkit itself — while Kaizen is a public concept, Danaher's version of DBS is a 40-year accumulation of practical tools carrying enormous tacit knowledge that cannot be replicated from a textbook. Layer two is DBS talent — practitioners who truly understand how to apply DBS in M&A integration contexts are extraordinarily scarce, and Danaher's development pipeline is the industry benchmark. Layer three — the deepest moat — is the track record of successful transformations: this record enables Danaher to show the next seller genuine evidence that "you will be measurably better under our ownership."

The trust paradox of "forced integration": why do acquired companies end up becoming DBS's most passionate advocates?

The most counterintuitive thing about DBS is not how effective it is — it is that acquired companies almost always become its true believers. This is the core trust mechanism of system-embedded M&A.

In 2011, Danaher acquired Beckman Coulter, a medical diagnostics equipment company, for $6.8 billion. Before closing, Beckman Coulter's management team was deeply uneasy — they worried about cultural disruption, brand dilution, and headcount reductions.

But after closing, the DBS team entered and began applying Kaizen methodology to Beckman Coulter's instrument service processes. The results: average service response time fell from 4.8 days to 2.1 days, customer satisfaction scores improved significantly, and the gross margin of the service business rose by 9 percentage points over three years.

The managers who had been most resistant at the outset became the most enthusiastic DBS advocates three years later. They shared their transformation stories at industry conferences. They used "DBS culture" as a recruiting pitch when hiring new talent.

There is a profound logic to this: people inherently resist being changed, but nobody resists becoming better. DBS is smart enough never to say "we are going to change your culture." It only asks: "What is your biggest source of waste right now? Let's eliminate it together." When employees solve a problem that has frustrated them for years using their own hands, they have not been conquered by Danaher — they have been conquered by the satisfaction of improvement itself.

Three trust models, three fundamental bets: what are Berkshire, CSU, and Danaher each wagering on?

Having covered the first three installments of this series, we now have three radically different trust-building paths. Placed side by side, the divergence becomes unmistakable.

| Dimension | Berkshire Hathaway Personality Trust |

Constellation Software Institutional Trust |

Danaher / DBS System-Embedded Trust |

|---|---|---|---|

| Source of trust | Buffett's personal commitment and reputation | 30 years of "never sold" behavioral track record | Post-transformation results — the numbers speak |

| Promise to acquired company | Permanent home; no management interference | Permanent hold; near-zero integration | We will make you measurably better |

| Integration intensity | Very low | Near zero | High (full DBS deployment) |

| Ideal asset type | Large-cap businesses with stable, durable moats | Small niche vertical market software | Industrial/science companies with improvement headroom |

| Speed of trust formation | Slow (requires long relationship accumulation) | Medium (requires time to validate the track record) | Fast but high-risk (6–18 months reveals the truth) |

| Greatest failure risk | Succession crisis (Berkshire = Buffett) | Low-quality assets with no exit path | DBS integration failure → cultural conflict |

| Replicability | Extremely difficult (personality capital is non-transferable) | Medium (requires years of track record) | Learnable — but demands heavy talent investment |

This comparison reveals a critical insight: no model is universally superior — only a model that fits your asset type and capability boundaries is correct.

Berkshire buys businesses that need no transformation, so non-interference is right. CSU buys niche software whose moat erodes under integration, so non-integration is right. Danaher buys industrial companies with improvement potential but no improvement tools, so deep integration is right.

The same behavior — to integrate or not to integrate — can be exactly right or catastrophically wrong depending on the asset type and context.

DBS as a screening tool: what kind of company would Danaher never buy?

Beyond its role as an integration tool, DBS has a function that is frequently overlooked: acquisition filter.

Danaher has an unwritten standard: it only buys companies where "DBS can add value." This standard is stricter than it appears on the surface.

✅ Meaningful improvement headroom — Visible waste in processes, unstable lead times, low inventory turns. These "problems" are opportunities to Danaher, not red flags.

✅ Predictable business model — Not a turnaround story, but a company with stable customers and recurring revenue that simply lacks operational efficiency.

✅ Service revenue streams — Instruments sold once, followed by recurring reagents, spare parts, and maintenance contracts. DBS improves service quality, which directly converts into customer retention.

❌ Will not buy cases requiring technology breakthroughs — DBS improves process efficiency, not R&D capability. If the problem is "the technology is not good enough," DBS cannot solve it.

❌ Will not buy culturally integration-resistant companies — This is a pre-deal due diligence priority. If management explicitly resists an improvement culture, Danaher typically walks away — regardless of how attractive the financial profile looks.

This filtering mechanism is why Danaher's deal success rate far exceeds the industry average. It is not betting "we can fix anything we buy." It is asking: "Is this company's problem the specific kind of problem that DBS can solve?"

The limits and risks of DBS: when does "system embedding" become cultural poison?

① High-intensity deployment is only justified when improvement headroom is large enough. For a company already running at high efficiency, DBS's marginal returns diminish rapidly. If Danaher forces DBS deployment simply to "give it something to do," the result is interference, not improvement.

② Cultural foundation determines how deeply DBS takes root. Manufacturing cultures, engineering-driven organizations, and process-oriented companies absorb DBS readily. Consumer brands, creative businesses, and talent-dispersed organizations tend to find DBS deployment far more painful. Part of the rationale behind Danaher's 2019 Dental segment spin-off (which became Envista) was that dental clinic culture was a poor fit with DBS rhythm and intensity.

③ Rapid expansion can outpace talent supply. Developing a genuine DBS Leader takes years of frontline practice — it cannot be accelerated. When Danaher completes multiple large acquisitions in quick succession (such as Pall Corporation in 2015 and GE Biopharma in 2020), the scarcity of qualified DBS practitioners becomes the binding constraint on integration quality.

④ The Fortive spin-off question: can DBS exist independently of Danaher? In 2016, Danaher spun off its industrial segment as Fortive, with DBS culture transferred along with it. Fortive's subsequent performance confirmed that DBS can be transplanted as organizational DNA — but also raised a question: when DBS becomes a shared language across multiple independent companies, does its scarcity value dilute?

The Taiwan lesson: it was never about lacking systems — it's about lacking the vision to imagine where M&A can take you

If you are a Taiwanese corporate executive reading this, you have probably already been frowning for several paragraphs:

"We already have all of this documented. Our ERP has been running for twenty years. Our SCM spans three continents. Our ISO certifications are stacked thick enough to use as a pillow. We have entire playbooks for managing currency risk under geopolitical uncertainty. Systems are not what we lack."

That reaction is exactly right. The root of the problem was never systems.

The real challenge for Taiwanese companies is vision — the ability to imagine, through a single M&A transaction, what you could become.

Organic growth asks: how do I do what I already do, better? M&A asks: how do I acquire a version of myself that does not yet exist? These are two fundamentally different starting points. Taiwanese companies are extraordinarily skilled at the first. They are almost strangers to the second.

Ambition and Capacity: Can You Hold a Larger Version of Yourself?

M&A is not purely a financial decision — it is a declaration about how large you are willing to become.

Taiwanese companies' growth DNA is almost entirely customer-driven: customers demand better yields, you improve processes; customers demand geographic diversification, you build factories in Vietnam and India; customers demand lower quotes, you compress costs. This is reactive growth — but it accumulates extraordinarily deep execution capability over decades.

M&A demands a different kind of ambition — one that does not wait for a customer directive, but instead asks: "If I owned this company, what could I become?" This requires executives to tolerate ambiguity, absorb higher failure risk, and accept responsibility for an organizational culture they did not build. That is not a technical challenge. It is a question of strategic character — and strategic character has to be deliberately cultivated.

Vision: Can You Picture a Version of Yourself That Does Not Yet Exist?

Vision is the ability to see beyond your current boundary.

On the supply chain dimension, Taiwanese executives have world-class vision — they know the geopolitical risk profile of every component, they know which port breaks down under which scenario, they know how currency volatility propagates through three layers of supplier cost structure. This systematic global awareness is a genuine competitive advantage.

But ask the same executives: "If you acquired a German industrial software company, what would you do with it?" — and they often go quiet. Not because they are not smart. But because they have never been required to think in this mode.

① What capability am I trying to acquire through M&A? — Technology? Brand? Distribution channel? Talent? A foothold in a market I cannot enter organically?

② What can I become when that capability combines with what I already have? — Not addition, but multiplication. A good acquisition should make 1+1 far greater than 2 — not simply give you another company to manage.

③ Where will I be in five years if I don't make this move? — What is the ceiling of organic growth? Have competitors already used M&A to build advantages I cannot close the gap on?

Taiwanese executives are rarely trained to answer these three questions systematically. That is the gap — and it is not a system gap.

Execution Strength: Taiwan's Greatest Asset, and Its Potential Trap

Here is an uncomfortable truth: Taiwanese companies' execution strength can sometimes become an obstacle to successful M&A.

Because they execute so effectively, some Taiwanese acquirers default to the "fix the obvious problems" mindset after closing — dispatching Taiwanese management teams, implementing Taiwanese operating processes, effectively converting the acquired company into an extension of a Taiwan factory. This approach works well in manufacturing management; in M&A integration, it frequently produces the opposite of the intended effect.

The acquired company has its own cultural assets. If you assume "the Taiwanese way is better" can resolve every issue, you will quickly discover: the best local talent leaves first, customer relationships begin to fray, and what you paid for becomes a hollow shell.

In an M&A context, true execution strength means knowing when to drive change and when to step back and let the acquired company remain itself. This requires not tighter control, but deeper tolerance.

Tolerance and Localization: Can M&A Go the Last Mile?

There is one aspect of DBS that rarely gets mentioned: DBS is not a refined version of a Taiwanese expatriate management model. It is a system designed to make local people at the acquired company the primary agents of improvement. The stars of a Kaizen event are the frontline employees of the acquired company — not the Danaher specialists who flew in.

That is the deepest meaning of tolerance in M&A: can you set down the superiority of "I know how to do this," and genuinely allow the talent at the acquired company to shine within the framework you provide?

As Taiwanese companies expand globally, the ultimate test is not whether they can identify good acquisition targets. It is whether, after closing, the local talent at the acquired company feels "this is my company — not a company that was bought by Taiwanese people." That step is localization. And localization's prerequisite is tolerance.

As Taiwanese companies enter the M&A era, they do not need to copy DBS's toolkit or lament that they lack "M&A genes." What they need is to systematically cultivate four capabilities:

Ambition (器識) — Proactively define "what we want to become," rather than waiting for customers to tell you. Make M&A a strategic anchor, not an opportunistic financial move.

Vision (眼界) — Imagination is itself a competitive advantage. The ability to see the strategic leverage in an acquisition — not just "what we're buying," but "what we can become after buying it."

Execution — Taiwan already has this. But redefine it for the M&A context. Not "transplanting the Taiwanese way," but "building a framework in which the acquired company's people improve themselves."

Tolerance and Localization — The last and hardest mile. After the acquisition, can you let local talent become owners — not subordinates of a Taiwanese expatriate team? Can employees at a European company say: "Our parent is Taiwanese, but they helped us become better versions of ourselves"?

Taiwanese companies do not lack systems. They do not lack capital. They do not lack the ability to execute. What they lack is the audacity to imagine a larger version of themselves — and the tolerance to let that larger self take genuine root in the world.

- Overview: Five M&A Models — After the Acquisition, Do You Choose Trust or Control?

- Part 1: Berkshire Hathaway — The Permanent Home Philosophy, Personality Trust at Its Peak

- Part 2: Amphenol — Institutional Trust, the Decentralized Self-Governance of 130 Business Units

- Part 3: Constellation Software — The Never-Sell Commitment, Platform Compounding Trust

- Part 4 (This Article): Danaher / DBS — System-Embedded Trust, Building Trust Through Transformation

- Part 5: Foxconn × Sharp — Vertical Chain Extension, the Price of Cultural Tension

- Part 6: Taiwan Steel Group — Opportunistic Composite Model, the Gains and Losses of Financial-Led M&A

- Conclusion: The Taiwanese M&A Manifesto — Integrity, Mutual Aid, Shared Success, Tenacity, Flexibility

Comments ()