Astera Labs (ALAB) Deep Research: The AI Connectivity Monopolist — or Is Valuation Already Overextended?

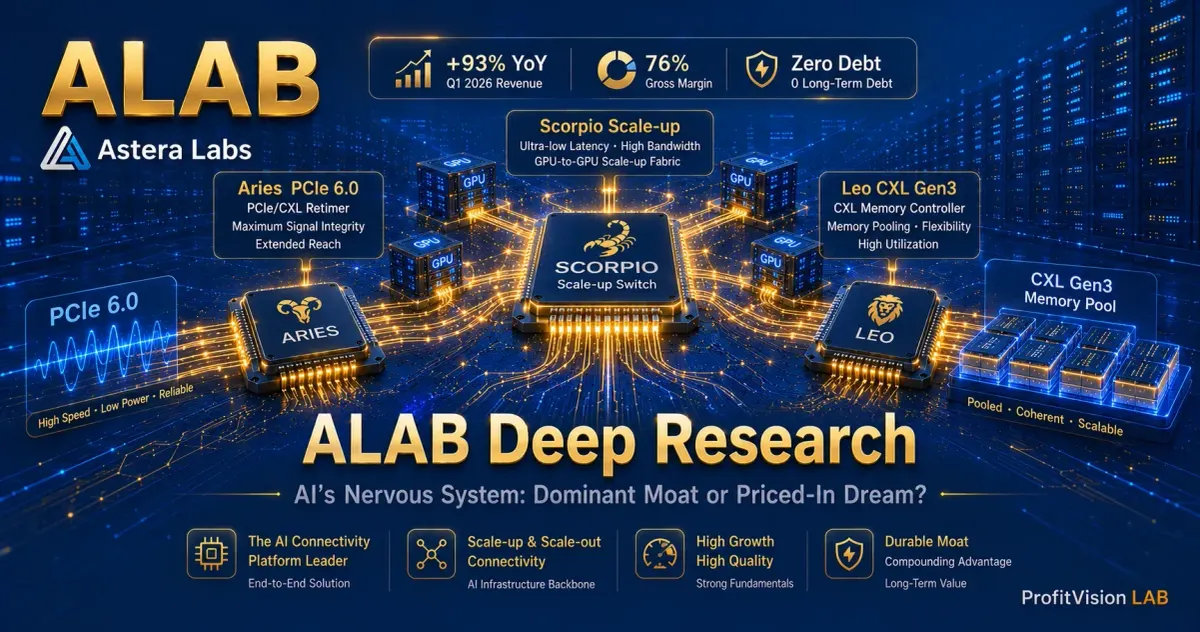

Astera Labs (ALAB) holds 50%+ PCIe 6.0 Retimer share, 76% gross margin, zero debt, and 93% YoY growth in Q1 2026. Scorpio Switch targets a $20B Scale-up market — but at 20x+ NTM EV/Rev, valuation has fully priced in success. Four-Filter verdict: Pass but Wait for a better entry.

76% gross margin, zero debt, 93% YoY growth — Astera Labs is the purest-play AI Infrastructure name with the clearest Economic Moat, but its valuation has already priced in 2027's dreams

2026.05.16 | Shiba the Disciplined | ProfitVision LAB | Last Updated: 2026.05.16

🔍 Four-Filter Quick Reference

| Filter | Metric | Data | Result |

|---|---|---|---|

| Filter 1: Institutional Flow | RS Rating / Institutional Ownership Trend | 93% YoY growth, institutional accumulation accelerating, strong momentum | ✓ Pass |

| Filter 2: Economic Moat | Gross Margin / ROE / Switching Costs | Gross margin 76.3%, ROE 16.1%, Gen 3 CXL, moat clearly defined | ✓ Pass |

| Filter 3: Volatility | IV Rank / Price Volatility | High-growth stock, elevated IV, options strategies require careful design | ⏸ Caution |

| Filter 4: Technicals | Trend / Valuation | Strong technical trend, but 20x+ EV/Rev valuation has fully priced in growth | ⏸ Wait for Pullback |

Chapter 1: Industry Map

This chapter answers: Where does Astera Labs fit in the AI Infrastructure landscape — and why is its role so critical?

PCIe (Peripheral Component Interconnect Express) is the high-speed bus standard used for communication between a CPU and GPUs, SSDs, and network cards on a server motherboard. Each PCIe generation roughly doubles the data rate: PCIe 4.0 (16 GT/s) → PCIe 5.0 (32 GT/s) → PCIe 6.0 (64 GT/s).

The challenge: the higher the data rate, the more signal attenuation and noise accumulate over copper traces — even over just a few centimeters, the signal begins to degrade. A Retimer (signal re-driver) sits in the signal path, fully receives the degraded signal and retransmits it cleanly, ensuring the GPU receives exactly what the CPU sent.

At PCIe 5.0 and below, many designs could rely on a simpler "Redriver (equalizer)" to compensate. But at PCIe 6.0 speeds, virtually every AI GPU server requires a Retimer — this is precisely why Astera Labs' Aries series has become a standard component in AI servers.

If GPUs are the neurons of an AI brain, Astera Labs' products are the synapses — transmitting signals between all compute nodes and ensuring the entire system operates as a unified whole rather than a collection of isolated compute islands.

The challenge for modern AI training clusters is no longer raw compute alone, but the connectivity bottleneck: when you connect 10,000 GPUs together, the efficiency of every data-transfer node between them determines the effective compute throughput of the entire cluster. Astera Labs' Intelligent Connectivity Platform is the specialized chipset and software platform purpose-built to solve this problem.

System Controller

ALAB Core Product

ALAB New Growth Engine

Compute Core

ALAB Third Pillar

ALAB's addressable market spans several key segments:

- PCIe Retimer Market: As PCIe Gen 5/6 adoption scales, Retimers are becoming a standard component on virtually every GPU server board. Estimated 2026 TAM exceeds $1B, with ALAB holding more than 50% share in PCIe 5.0/6.0 Retimer.

- Scale-up Switching Market: Scorpio X-Series targets an estimated $20B+ AI interconnect switch market, beginning to ramp in 2026.

- CXL Memory Market: Leo series addresses the AI system "memory wall" problem — large long-term potential but slower adoption timeline.

Chapter 2: Business Model & Economic Moat

The Economic Moat is ALAB's central investment thesis. Let's dissect it layer by layer.

2.1 Product Matrix

Industry-standard position, PCIe 6.0 first mover, standard component in every GPU server, primary revenue driver through 2025

Biggest growth engine for 2026; 320-lane X-Series targets AI cluster interconnect; management expects it to become the largest product line

Gen 3 CXL controller while competitors are still at Gen 1. Solves GPU memory sharing problem

CXL (Compute Express Link) is an open-standard interconnect protocol built on top of the PCIe physical layer, co-developed by Intel, AMD, ARM, NVIDIA, and other major vendors. Its defining feature is enabling memory pooling across CPUs, GPUs, and accelerators — multiple processors can access the same physical memory without copying data.

During AI training, large language models (LLMs) frequently exceed the HBM capacity of a single GPU. The traditional solution is to shard the model across multiple GPUs, incurring heavy data-movement overhead. CXL enables memory "pooling" — multiple GPUs share one large memory pool, dramatically reducing data-movement latency and power.

Astera Labs' Leo CXL controller is now at its third generation, while competitors (Marvell, Microchip, etc.) are mostly still on their first generation. This generational lead, when the technology adoption curve accelerates, will translate into a substantial first-mover advantage.

In-rack short-reach 800G Ethernet smart cable module — more cost- and power-efficient than optical solutions

2.2 Economic Moat Identification

🏛 Switching Costs (Strong): The Aries series is deeply embedded in hyperscale data center server board designs. The COSMOS software platform provides unified management and debugging tools across product lines — once adopted, switching costs are extremely high. This is not a single-chip swap; it's a wholesale replacement of an integrated hardware-software ecosystem.

🏛 First-Mover Advantage (Strong): Leo CXL controller is at Gen 3 while most competitors are still on Gen 1. Aries 6 for PCIe Gen 6 is already in mass production while Broadcom and Marvell play catch-up. Each chip generation involves a 12-18 month design integration cycle — first movers enjoy a structural protection window built into that timeline.

🏛 Depth of Focus (Strong): Astera Labs is 100% focused on data center connectivity chips — this allows product iteration speed to outpace diversified incumbents. Broadcom has dozens of product lines; Marvell does too. But ALAB does only one thing: make AI cluster connections faster and more power-efficient.

⚠ Moat Vulnerability: The Bundling Threat

Broadcom can package PCIe Switch and Retimer together, offering a "single-vendor, single-debug-tool" solution. The common configuration today is still Broadcom PCIe Switch + ALAB Retimer — but Broadcom is now pushing its own Retimer, attempting to close this combination exclusively. This is ALAB's biggest Economic Moat vulnerability.

Chapter 3: Competitive Landscape

ALAB's competitive landscape is more complex than MXL's — it faces competition from multiple directions, and every competitor is far larger than itself.

| Competitor | Competing Products | Threat Level | ALAB's Defense |

|---|---|---|---|

| Broadcom (AVGO) | PCIe/CXL Retimer, PCIe Switch | High (Bundling) | COSMOS software ecosystem, Gen 6 first-mover, customer stickiness |

| Marvell (MRVL) | PCIe Retimer, CXL Controller | Medium | Generational lead (Leo Gen 3 vs. MRVL Gen 1) |

| Microchip / Rambus | CXL Memory Controller | Medium (Long-term) | Leo's generational technology lead is significant |

| NVIDIA (in-house) | NVLink Fusion Integration | Medium (Specific Scenarios) | ALAB supports NVLink Fusion; cooperative relationship |

| Credo (CRDO) | PCIe Retimer (partial overlap) | Low (Current) | CRDO's focus is AEC — a different lane |

3.1 Scorpio: The Bet on a $200B Market

Scale-out (horizontal scaling) means adding more independent nodes (servers/racks) to increase total compute capacity, with nodes interconnected over long-range Ethernet or fiber. This is the dominant architecture for traditional data centers and suits inference workloads.

Scale-up (vertical scaling) means enabling multiple GPUs within the same cluster to communicate directly with each other — sharing memory and compute resources and behaving like one giant "virtual GPU." This is the essential architecture for large-model training: 10,000 GPUs training a GPT-5-class model need all GPUs to coordinate with microsecond-level latency, and only a Scale-up interconnect can deliver that.

NVIDIA monopolizes Scale-up interconnect within its own GPU ecosystem via NVLink. But AMD, Google TPU, and hyperscale customers who prefer open standards need a neutral third-party solution — that is Astera Labs Scorpio's market opportunity.

Scorpio X-Series is ALAB's most important growth bet. Scale-up interconnect for AI clusters — enabling GPUs within the same cluster to communicate directly at high speed — is the hottest area of demand right now. NVIDIA monopolizes Scale-up within the NVIDIA GPU ecosystem via NVLink, but AMD, Google TPU, and open-standard hyperscale clusters need a neutral third-party Scale-up Switch.

Scorpio targets the UALink (an open standard championed by AMD and others) Scale-up Fabric, as well as large-scale PCIe/CXL-based interconnect. Management expects Scorpio to become the company's largest product line by end of 2026, with the 320-lane X-Series already in production and shipping.

Chapter 4: Financial Resilience

ALAB's financial statements are the cleanest among these four companies. The numbers speak for themselves.

4.1 Explosive Revenue Growth

| Period | Revenue | YoY | Notes |

|---|---|---|---|

| FY 2023 | ~$164M | — | Pre-IPO scale |

| FY 2024 | $396M | +141% | Post-listing breakout |

| FY 2025 | $852.5M | +115% | Aries in full mass production |

| Q1 2026 | $308.4M | +93% | PCIe 6 > 1/3 of revenue |

| Q2 2026E | $355-365M | ~+70%E | Management guidance, well above consensus |

| FY 2026E | $1.3-1.5B | ~+58%E | Analyst consensus estimate |

4.2 Profitability — Best-in-Class

| Metric | FY 2024 | FY 2025 | Q1 2026 |

|---|---|---|---|

| Gross Margin | ~73% | 75.7% | 76.3% (Non-GAAP) |

| Non-GAAP Operating Margin | ~28% | ~33% | 36.2% |

| Net Income (GAAP) | Loss period | $174M+ | $80.3M |

| ROE | — | 16.1% | Expanding |

| ROIC | — | ~9.2% | Improving |

Fabless (fabrication-less design) means the semiconductor company handles only chip design — it does not own a fab, outsourcing manufacturing to foundries like TSMC or Samsung. Companies that own their own fabs are called IDMs (Integrated Device Manufacturers), such as Intel or Samsung.

The Fabless model's advantage: no need to carry the enormous capital expenditure of a wafer fab (often in the billions), so 100% of company resources can focus on R&D and customer relationships. As a result, Fabless companies typically maintain higher gross margins (50-80%), while IDMs with their own fabs tend to run lower (40-60%).

Astera Labs' 76% gross margin is the result of three layers stacked together: the Fabless model + highly customized chips (competitors cannot replicate quickly) + COSMOS software platform (adds differentiated value on top of hardware).

A 76% gross margin is top-tier for the chip design industry — reflecting the compounded effect of: Fabless model + highly customized chips + software-added value. With Scorpio scaling, gross margins are likely to remain stable or expand further.

⚠ Note: Q2 2026 gross margin guidance is approximately 73%, including ~200bps of non-cash amortization from new customer warrants. This is a one-time financial structure adjustment, not a sign of business model deterioration.

4.3 Balance Sheet — The Cleanest Among Peers

| Item | FY 2025 |

|---|---|

| Cash & Equivalents | $167.6M |

| Long-term Debt | $0 |

| Shareholders' Equity | $1.0B |

| D/E Ratio | 0% |

Zero debt, ample cash, sustained profitability — this is the most financially resilient balance sheet among peer companies. Even if AI capex enters a temporary slowdown, ALAB has sufficient financial buffer to weather it.

Chapter 5: Valuation & Scenario Analysis

Valuation is ALAB's only concern. Company quality is not in question — the market already knows that.

Current ALAB NTM EV/Revenue is approximately 20-25x, placing it in the high-end tier of growth semiconductors. This multiple implies the market expects 58%+ annual revenue growth to continue through 2027.

| Scenario | Core Assumption | FY 2027E Revenue | Reasonable EV/Rev | Market Implication |

|---|---|---|---|---|

| 🟢 Bull Case | Scorpio becomes the standard Scale-up choice for AI clusters; Leo CXL sees broad AMD GPU ecosystem adoption; PCIe 7 design win rate high | $2.5B+ | 25-30x | Current valuation fair or even cheap; the key debate is whether Scorpio establishes market leadership |

| 🟡 Base Case | Scorpio ramps on schedule, becomes largest product line by year-end; Aries maintains PCIe 6 dominance; Broadcom bundling partially erodes but not fatal | $1.8-2.0B | 18-22x | Current stock price roughly fair; pullbacks offer better entry opportunities |

| 🔴 Bear Case | Broadcom bundling materially erodes Aries share; Scorpio adoption slower than expected; AI capex cycle turns down | $1.2-1.4B | 12-15x | Current stock price significantly overvalued; 30-40% drawdown risk |

Current market pricing reflects a Base Case skewing toward Bull, with zero margin of safety built in for execution risk. For investors already holding a position, the thesis remains clear. For those not yet positioned, waiting for a better entry point — during market-wide panic or a broader correction — is the more rational choice.

Chapter 6: Conclusion & Tactical Recommendations

Core Thesis

Astera Labs is the highest-quality, clearest-moat pure-play in the AI Infrastructure connectivity chip market. The only issue is valuation — its stock has fully priced in success, leaving no room for any execution misstep.

✓ Bull Case (Three Pillars)

- Scorpio Opens a Second Growth Curve: Aries is already a mature high-growth business. Scorpio ramping to mass production in H2 2026 means ALAB is entering the $20B switch market. If Scorpio establishes its position, 2027 revenue could exceed current consensus.

- CXL Long-Game Positioning: Leo Gen 3's technology lead in CXL provides the most capable hardware acceleration platform for the AI memory architecture transition. Once the CXL adoption curve accelerates, Leo's addressable market will explode.

- Financial Flywheel: Zero debt + 76% gross margin + sustained profitability allows ALAB to continuously invest in R&D without diluting shareholders, maintaining its generational technology lead.

🚨 Bear Case (Three Risk Factors)

- Broadcom Bundling Threat: Broadcom's strategy of packaging PCIe Switch and Retimer together is ALAB's hardest-to-defend risk. If hyperscale data centers tilt toward full Broadcom stack purchases, ALAB's market share faces real erosion.

- Valuation with No Margin of Safety: At 20x+ NTM EV/Revenue, any quarter of even slightly below-consensus results — or a growth guidance cut — could trigger a sharp stock correction.

- AI Capex Cycle Risk: If hyperscale data center build-out pace slows (driven by ROI pressure or shifting competitive dynamics), ALAB's growth rate will be directly impacted, and current valuation has no buffer for that scenario.

Options Strategy Framework (Bull Put Spread Logic)

ALAB is a textbook example of a Four-Filter Defense Screen "Pass but Wait" verdict. Entry framework:

- Wait for a 10-15% broader market pullback, or a post-earnings sentiment overreaction entry

- Bull Put Spread: after pullback confirms support, sell ATM-10% Put, buy ATM-20% Put

- Time frame: use earnings cycles as anchor points; avoid selling puts immediately around earnings when IV is elevated

- Q2 2026 earnings (August 2026) is the most important Scorpio progress verification event

Trigger Conditions

| Situation | Condition | Action |

|---|---|---|

| Add Signal | Scorpio quarterly revenue beats + new hyperscale customer + stock pulls back to reasonable EV/Rev 15-18x | Build position aggressively; use pullback as basis for staged entry |

| Hold | Results in line with expectations, Scorpio on track, valuation stays in 18-22x range | Hold position, wait for better add-on opportunity |

| Downgrade to Watch | Clear Broadcom bundling erosion signals / Scorpio adoption below Q2 guidance / gross margin falls below 72% | Trim or stop adding; reassess Economic Moat strength |

📋 Tracking Log

| Date | Event | Judgment | Outcome |

|---|---|---|---|

| 2026/05/16 | Initial publication, based on Q1 2026 earnings | ✓ Pass — waiting for entry point | — |

Next scheduled update: After Q2 2026 earnings (August 2026)

Early update triggers: Scorpio major customer announcement / Broadcom bundling competitive event / Significant valuation correction (-20%+)

FAQ

Over fifteen years of deep expertise in US equity options strategy and industry research. Uses the "Four-Filter Defense Screen" to systematically evaluate individual stock operability, with continuous coverage of PCIe, CXL, and Scale-up interconnect technology cycles. This research is based on public filings, SEC documents, and Astera Labs official investor materials. It does not constitute investment advice.

Investing involves risk. Please evaluate carefully based on your own financial situation.

Data sources: Astera Labs SEC Filings, Q1 2026 Earnings Call Transcript, SemiAnalysis, Futurum Research, public information (as of May 2026)

Comments ()