AI High-Speed Connectivity Chips: The Four-Way Battle Between MRVL, CRDO, MXL & ALAB

The AI data center buildout is reshaping connectivity chip markets. Marvell dominates optical interconnect, Credo owns active electrical cables, MaxLinear challenges in PAM4 DSP, and Astera Labs holds a PCIe moat. This industry overview maps all four competitive layers.

From 800G to 1.6T — an arms race for control of the AI cluster's nervous system. A complete breakdown of the Economic Moat, technology tracks, and Investment Framework for all four companies.

2026.05.16 | Shiba the Disciplined | ProfitVision LAB | Last Updated: 2026.05.16

📚 Series Navigation

Chapter 1: Why Connectivity Chips Deserve More Attention Than GPUs

Every AI investor knows NVIDIA. But those who truly understand AI clusters shift their focus to connectivity chips.

In an AI training cluster powered by 10,000 H100 GPUs, the ceiling on total compute throughput is determined by the slowest connectivity node. No matter how fast the GPUs themselves are, if the data transmission channels lack sufficient bandwidth efficiency, the entire cluster falls into a "compute traffic jam" — like an eight-lane expressway that narrows to two lanes at the toll booth.

That bottleneck is exactly where the connectivity chip investment opportunity lives. And the competitive logic in this market is more nuanced and differentiated than GPUs themselves — because it spans multiple distinct technology layers, each with its own Competitive Landscape and Economic Moat structure.

"The speed limit of an AI cluster is not determined by the GPU. It is determined by every single chip that connects the GPUs."

1.1 Market Size: Bigger Than You Think

The global optical module market surpassed $23 billion in 2025, and is expected to sustain 25%+ annual growth into 2026. When you add PCIe interconnects, CXL memory controllers, active electrical cables, and Scale-up Switches — the full "AI cluster connectivity layer" TAM — Marvell has publicly stated the total data center semiconductor TAM could approach $100 billion by 2028.

The four companies covered in this series alone are expected to generate a combined FY2026 revenue exceeding $3 billion, all accelerating. This is a market transitioning from "mature" to "exponential growth."

| Connectivity Layer | Technology Standard | 2026E TAM | Growth Driver |

|---|---|---|---|

| Optical Interconnect DSP | PAM4 800G / 1.6T | $3–5B | Inter-rack fiber expansion in AI clusters |

| Active Electrical Cable (AEC) | 224G SerDes | $2–3B | Short-reach high-density intra-rack interconnect |

| PCIe Retimer / Switch | PCIe Gen 5/6 | $1–2B | Standard component in every AI server board |

| Scale-up Switch | UALink / NVLink / PCIe | $5–20B (long-term) | Intra-cluster interconnect for 10,000+ GPU clusters |

| CXL Memory | CXL 2.0 / 3.0 | $1–3B (2027+) | AI memory wall solution |

800G means a single optical module transfers data at 800 Gigabits per second (= 100 GB/s). Inside an AI data center, a single GPU server may need to transfer several terabytes of gradient data per second to other GPUs, and aggregate rack-level traffic can easily reach petabit-per-second scale. 800G is the dominant standard in 2025–2026, but large-scale clusters are already pushing beyond it.

1.6T (Terabit) is the next-generation specification — twice the throughput of 800G. It is achieved either by increasing per-lane speed from 100G/lane to 200G/lane (requiring more advanced EML lasers) or by increasing lane count (16 × 100G = 1.6T). 2026 marks the first year of volume 1.6T production, with forecasts exceeding 5 million 1.6T module shipments for the year.

Every speed generation transition triggers a full re-certification cycle across the entire supply chain — chip vendors (DSP), module makers (optical OEMs), and data centers (system integration) all must re-select their partners. That is why "who reaches volume production first in the 1.6T era" matters so much.

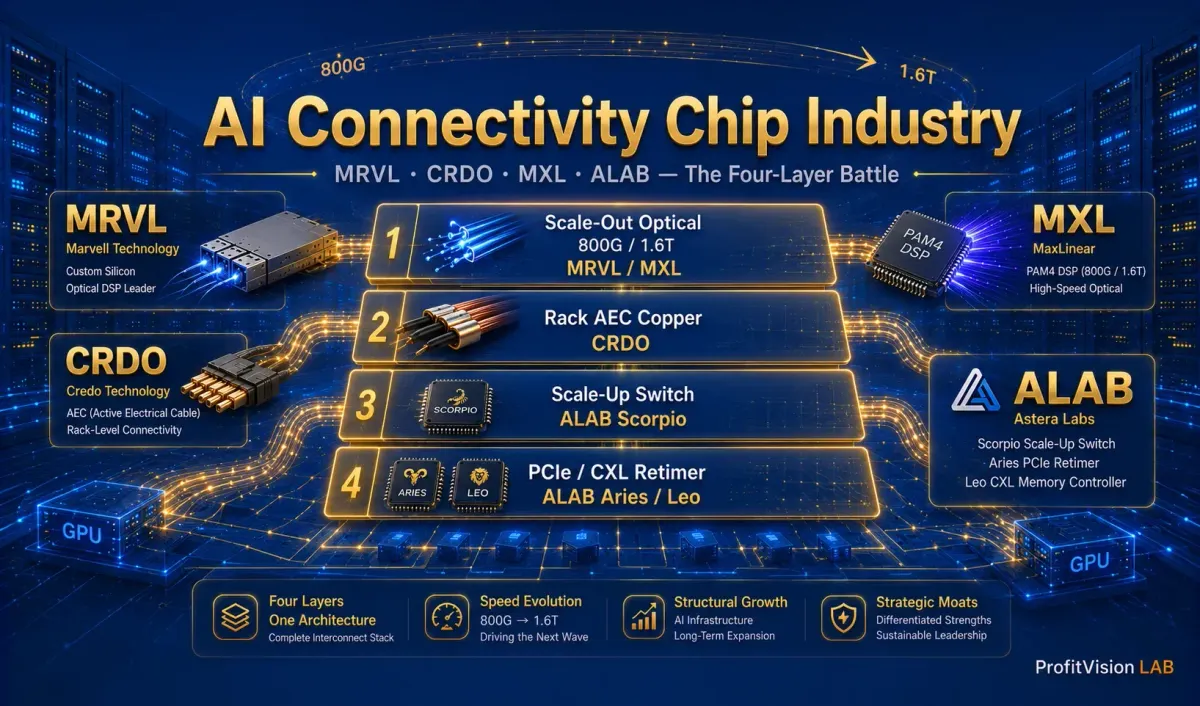

Chapter 2: The Connectivity Topology of an AI Cluster

To understand each company's positioning, you first need to understand the physical architecture of an AI cluster. In a modern hyperscale data center, connectivity chips play roles distributed across distinct layers as follows:

Inter-rack / Inter-cluster

PAM4 DSPs convert electrical signals to optical signals, connecting GPU servers across different racks and even different buildings. This layer carries the highest traffic volumes and longest distances, and is the first bottleneck hit when scaling an AI cluster.

Short-reach High-density

GPUs within the same rack or adjacent racks are connected via active electrical cable. Cheaper than optical fiber, more power-efficient, and cost-effective. Credo holds a dominant position at this layer.

Intra-cluster GPU Direct Connect

Allows GPUs within the same cluster to operate as a single, unified compute unit. NVIDIA dominates its own ecosystem with NVLink; open-standard UALink creates opportunities for third parties. This is the hottest growth track for 2026–2027.

CPU-GPU Signal

PCIe signals between CPUs and GPUs degrade at high speeds; Retimers regenerate the signal mid-path. Required in every AI server — now a standard component.

CXL Shared Memory

Enables multiple CPUs/GPUs to share a common memory pool, solving the AI "memory wall" problem. The most technically advanced layer, still early on the adoption curve, but with enormous long-term potential.

AEC (Active Electrical Cable) is a high-speed connectivity solution that integrates a SerDes chip at each end of a copper cable. Copper cable alone has limited reach (typically under 3 meters), but the SerDes chips in an AEC actively compensate for signal degradation, enabling the copper cable to support 400G or even 800G transmission speeds.

Compared to optical fiber: AEC is significantly cheaper (roughly 30–50% of the cost of an optical module), more power-efficient (no optical-electrical conversion loss), and lower latency. The tradeoff is distance — AEC is limited to 3 meters and is only suitable for intra-rack or adjacent-rack short-reach interconnects. Optical fiber handles inter-rack and inter-building long-reach transmission.

In a typical AI data center deployment, AEC connects GPUs within the same rack while optical fiber connects GPUs across different racks. Credo (CRDO) holds an overwhelming technology and market share advantage in the AEC market — this is its core Economic Moat.

Chapter 3: The Four-Way Battle — Strategic Analysis of Each Player

🔷 Marvell (MRVL): Dominant Player in Optical Interconnects, Moving to a Higher Dimension

Marvell is the only company among these four that can genuinely be called a "full-stack connectivity chip platform." Its Ara series 800G/1.6T PAM4 DSP has become the market standard, its Electra coherent DSP extends deep into long-haul backbone networks, and its custom ASIC (XPU) business puts it directly inside the hyperscale data center custom chip design process.

In FY2026 Q3 (through early 2026), the data center business accounted for 73% of MRVL's total revenue, and is still accelerating. The company's full-year revenue reached $7.7B, the largest scale among the four.

Marvell's strategic positioning: at every speed-generation transition, be the first commercial option to reach volume production. In the 1.6T era, MRVL has already achieved that — cementing its first-mover advantage. Its Economic Moat derives from three dimensions: technology breadth (DSP + coherent + custom ASIC), scale advantage ($7.7B in engineering firepower), and deeply embedded relationships with hyperscale data center customers.

MRVL's weakness lies in valuation — the market has already priced in its growth trajectory, and the larger it gets, the harder it becomes to sustain high growth rates.

🟢 Credo Technology (CRDO): AEC Market Leader, Evolving Into a Full-Spectrum Player

Credo's core story is that of a company starting from a niche market (AEC active electrical cable), leveraging technical depth and customer stickiness to expand progressively into a broader connectivity chip footprint.

In the AEC (Active Electrical Cable) market, CRDO is the undisputed market leader. AEC is the optimal solution for short-reach intra-rack and adjacent-rack interconnects in AI clusters — cheaper than optical fiber, more efficient than passive copper, and the standard choice in the 800G era. CRDO's SerDes technology leads the industry in power efficiency and signal integrity, and once a major hyperscale data center integrates its solution, switching costs make a supplier change almost unthinkable.

CRDO's FY2026 estimated revenue growth is approximately 120% — the most explosive among the four. More importantly, it is expanding into five new pillars: Cardinal 3nm optical DSP, Zero-Flap Optics, ALC (Active Line Cable), OmniConnect gearbox, and IC solutions (Retimer). These five new fronts expand CRDO's TAM from a few hundred million dollars to over $10 billion.

CRDO's risks: AEC market growth depends on continued AI cluster expansion, and Cardinal DSP — as a new entrant — faces stiff design win competition from MRVL and MXL, both of which have proven volume production track records in optical.

🟣 MaxLinear (MXL): The Dark Horse of Optical DSP — Is the Valuation Discount an Opportunity or a Trap?

MaxLinear is the most dramatic transformation story among these four. In 2023, it was a broadband chip company struggling through a cyclical trough, with a failed acquisition (Silicon Motion) and revenue cut in half. By 2026, its Keystone PAM4 DSP has been adopted by multiple hyperscale data centers, and its infrastructure business grew 136% year-over-year in Q1 2026, becoming the company's largest segment.

MXL's core thesis is the "third-pole" argument — beyond the MRVL and Broadcom duopoly, hyperscale data centers need supply chain diversification, making them willing to cultivate a third commercial PAM4 DSP vendor. Keystone's 5nm solution has validated this thesis.

But here is the critical question for MXL: in the 1.6T era, MRVL has already achieved volume production, while Rushmore (MXL's 1.6T solution) is still in the chase. Every speed-generation transition is a re-certification war. Whether MXL can retain its hyperscale customer seat in the 1.6T era is the single most important monitoring metric over the next 12–18 months.

On valuation: NTM EV/Revenue of approximately 8x, a 50–60% discount versus CRDO (17x) and ALAB (20x+). This discount prices in the market's uncertainty about MXL's transformation — and is precisely where the opportunity lies. If Rushmore succeeds, the valuation gap will converge rapidly.

🟠 Astera Labs (ALAB): Monopolist of the PCIe Nervous System, Building an Economic Moat in a Different Dimension

The fundamental difference between Astera Labs and the other three: it does not make optical interconnect DSPs. Its battlefield is "all protocol connectivity between compute and storage" — PCIe Retimer (Aries), CXL memory controller (Leo), and Scale-up Switch (Scorpio).

In the PCIe Retimer market, ALAB's Aries series commands over 50% market share, and Aries 6 for PCIe 6.0 has already reached volume production — at least one technology generation ahead of competitors. The Leo CXL controller is the only third-generation product in the industry, while Broadcom and Marvell are only entering their first generation.

Q1 2026 ALAB revenue was $308.4M, up 93% year-over-year, with gross margin of 76.3% and zero debt. Financial quality is the highest of the four, and its Economic Moat is the clearest — the COSMOS software ecosystem creates deep customer dependency that goes far beyond the switching cost of a chip replacement.

Scorpio Scale-up Switch is ALAB's second growth curve — and its biggest bet. If the open-standard AI Scale-up interconnect market (UALink, etc.) reaches scale, the TAM for Scorpio's segment could exceed $20 billion, far larger than the current PCIe Retimer market.

ALAB's weakness is valuation — 20x+ NTM EV/Revenue already prices in success. Any execution misstep could trigger a sharp correction.

Chapter 4: The Four-Way Comparison — Economic Moat, Financials, and Valuation Matrix

4.1 Company Quick Scorecard

4.2 Economic Moat Strength Matrix

| Moat Dimension | MRVL | CRDO | MXL | ALAB |

|---|---|---|---|---|

| Technology Generation Lead | Strong (Full-Stack) | Strong (AEC) | Medium (Catching Up) | Strong (PCIe/CXL) |

| Customer Switching Cost | Strong | Strong (AEC) | Medium (Transition Risk) | Strong (COSMOS Software) |

| Scale & Engineering Capacity | Strong ($7.7B) | Medium (~$0.6B) | Medium (~$0.64B) | Medium (~$1.4B) |

| Track Uniqueness / Moat Exclusivity | Medium (AVGO Competing) | Strong (AEC Dominant) | Weak (#3 Position) | Strong (PCIe 6 Dominant) |

| Financial Health | Strong | Strong | Weak (Still Unprofitable) | Strongest (Zero Debt) |

| Valuation Margin of Safety | Low (12–14x) | Medium (17x) | High (8x) | Low (20–25x) |

Chapter 5: Technology Roadmap — 800G Today, 1.6T Tomorrow

Understanding the technology cycle is the key to understanding the Investment Framework and timing for this sector.

Chapter 6: Investment Framework — Risk-Reward Matrix for All Four Companies

Placing all four companies into a unified investment decision framework:

| Company | Core Investment Thesis | Primary Tail Risk | 12-Month Catalyst | Recommended Strategy |

|---|---|---|---|---|

| MRVL | Full-stack optical interconnect platform + 1.6T first-mover + custom ASIC flywheel | Valuation compression; in-house chips eroding commercial market | 1.6T production validation; FY2027 guidance raise | Build position on pullbacks; core holding |

| CRDO | AEC market leader + Cardinal DSP opens second growth curve | Cardinal design win delays; hyperscaler customer concentration | Cardinal's first hyperscale design win announcement | Core position during growth explosion; sell Puts on high-IV days |

| MXL | Valuation discount + Rushmore 1.6T catch-up narrative + broadband recovery | Rushmore delays; hyperscale customer loss | Rushmore production announcement; Q2 optical upside surprise | Small position now; upgrade after Rushmore success confirmed |

| ALAB | Deepest PCIe/CXL Economic Moat + Scorpio opens $20B market | Broadcom bundling; no valuation margin of safety | Scorpio becomes largest business line; Q2 guidance beat | Wait for 10–15% pullback; highest quality, can build larger position |

6.1 Scenario Analysis: Which Macro Environment Favors Whom?

🟢 Bull Case: AI Capex Continues to Accelerate

If hyperscale data center build intensity sustains the pace seen in 2025–2026, all four companies benefit. Biggest beneficiaries: CRDO (fastest growth) and MXL (largest valuation expansion potential). ALAB and MRVL maintain solid growth but upside is limited by already-priced-in valuations.

🟡 Base Case: AI Build Stable but Not Accelerating

800G continues as the mainstream standard while 1.6T penetrates gradually. MRVL and ALAB sustain strong performance driven by Economic Moat depth. CRDO is supported by ongoing AEC orders. MXL depends more on individual stock narrative around Rushmore than sector tailwinds.

🔴 Bear Case: AI Capex Slowdown or Bubble Correction

Most vulnerable: MXL (still unprofitable, thin financial buffer) and the highest-valued ALAB. CRDO's AEC customer stickiness provides relative defensiveness. MRVL's scale and business diversity offer a cushion, but with data center at 73% of revenue, it cannot fully escape the impact. AI capex is the shared fate driver for all four.

Chapter 7: Conclusion — Understanding the Differences Is What Leads to the Right Decisions

"In the AI connectivity chip sector, the most common investment mistake is not picking the wrong company — it is applying the wrong analytical framework. Comparing ALAB to CRDO on growth rate, or MXL to MRVL on Economic Moat depth, are both errors of benchmark."

The differences among these four companies are fundamentally differences in technology layers:

MRVL is the dominant player in optical interconnects — its full-stack platform and 1.6T first-mover advantage build a durable Economic Moat. It is the "safest" large-cap name in this sector, but also the one least likely to deliver valuation surprises on the upside.

CRDO is the AEC market leader with the fastest current growth rate. Cardinal DSP is the decisive factor in whether it can evolve from a niche player into a full-spectrum competitor. Its risk-reward ratio is the most attractive of the four, but investors must tolerate customer concentration volatility.

MXL is the cheapest-valued transformation play. Rushmore is a clear binary event — success means rapid valuation discount convergence; failure means the transformation narrative collapses. Suitable for investors able to monitor technical progress and absorb volatility.

ALAB has the deepest Economic Moat and the healthiest financials of any pure-play in this group, but valuation already prices in success. The best strategy is to "wait for the market to offer a more reasonable entry point" rather than chasing. If Scorpio succeeds, ALAB has the highest growth ceiling of the four.

Finally, the most important shared characteristic of these four companies is that they all sit atop a structural, long-term growth trend: exponential growth in AI compute means every node that connects that compute must evolve at the same exponential pace. This trend is not a one-quarter trade — it is a five-year industry transformation.

① Switching Cost: Once a customer integrates a chip, replacing it requires redesigning the circuit board and re-running full certification and testing — extremely costly. ALAB Aries and CRDO AEC both fall into this category.

② Technology Generation Lead: Your product is in its third generation while competitors are still on generation one. ALAB Leo CXL controller is the clearest example — a multi-generation lead during a new technology adoption phase is a powerful Economic Moat.

③ Scale Advantage: The larger the scale, the more R&D cost can be amortized. Marvell's $7.7B in annual revenue gives it an overwhelming engineering resource advantage over MXL.

④ Software Ecosystem (Software Moat): When hardware gaps close, the software platform becomes the stickiness driver. ALAB's COSMOS creates customer dependency on its debugging tools and management ecosystem — far beyond the switching cost of replacing a chip alone.

⑤ First-Mover Design Win: Hyperscale data center vendor selection cycles last 12–18 months; once chosen, a supplier receives sustained purchase orders. MRVL's volume production lead in 1.6T is accumulating exactly this type of advantage.

FAQ

15+ years in US equity options strategy and industry research. This series covers in-depth individual stock research on all four companies — Marvell (MRVL), Credo (CRDO), MaxLinear (MXL), and Astera Labs (ALAB). All data is sourced from public financial filings, SEC filings, and earnings call transcripts. Analysis cutoff date: May 16, 2026.

Investing involves risk. Please evaluate carefully based on your own financial situation.

Data sources: SEC filings and earnings call transcripts from each company; Marvell / Astera Labs / MaxLinear / Credo Technology official IR websites; SemiAnalysis; Futurum Research; Mordor Intelligence; TSPASemiconductor; publicly available research reports (as of May 2026).

Comments ()