ServiceNow 重倉轉型:Put → 股票 → Covered Call → LEAPS

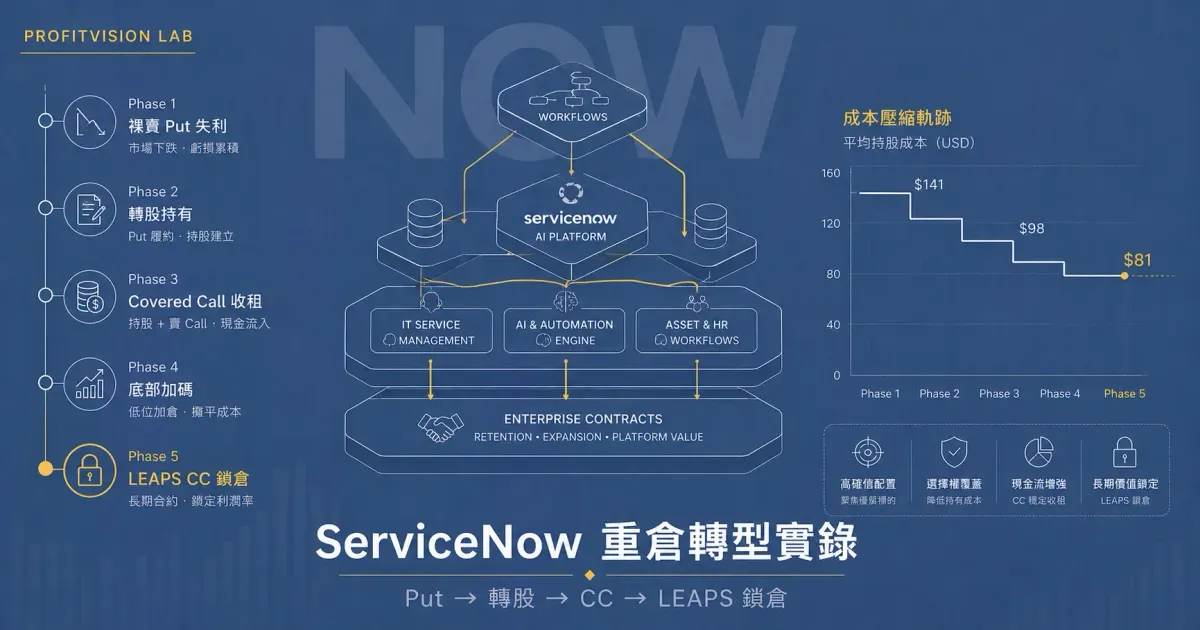

ServiceNow(NOW)重倉五階段完整記錄:裸賣 Put 失血 -$2,665、以 $128 設計成本轉股、Covered Call 收租、4 月逆勢加碼至 300 股、財報後賣出 LEAPS CC 收取 $5,247,持股成本從 $98.78 壓縮至 $81.28。每個決策背後都有明確邏輯。

ServiceNow 重倉轉型實錄

Put 失血 → 轉股 → Covered Call → LEAPS 鎖倉

這篇文章記錄的不是一個乾淨的成功案例,而是一個完整的「策略演進過程」——從失誤中學習,在市場的考驗中不斷調整框架,最終形成一個多層次的持倉管理系統。

ServiceNow(NOW)是全球企業 IT 服務管理的龍頭軟體公司,護城河深厚,但估值彈性大,財報前後常有劇烈波動。我在 2026 年初以選擇權為切入點,歷經五個清晰的階段演進,最終建立起一個以「深度研究 + 選擇權成本壓縮」為核心的重倉框架。(→ NOW 制度化建倉框架 v2.1)

📊 ServiceNow 財報時間點

Q4 FY2025 財報:約 2026 年 1 月 22 日 — 財報前後選擇權活動異常密集,股票從 $145 區域急跌至 $114,是這個故事的觸發點。

Q1 FY2026 財報:約 2026 年 4 月 23 日 — 恰好是大舉加碼後的當天,也是賣出 LEAPS Covered Call 鎖定策略的時點。

這篇文章記錄的很多操作——逆勢重倉、在急跌中大量加碼——從外面看可能像是違反紀律的情緒化接刀。但這些決策有一個讀者看不到的背景:我追蹤 ServiceNow 已經七、八年了。不只是讀財報,而是長期觀察它的業務週期、管理層執行力、護城河如何一年一年加深。

這種積累讓我在市場最恐慌的時候,對「這家公司是否還在」有一種量化難以完全表達的判斷力。同樣的邏輯,也適用於我在 CME、CBOE、IBKR 的操作——那些也是我長期使用、深度追蹤的金融基礎設施公司,我不只是研究他們,我每天都活在他們的產品裡。

沒有這個前提,這篇文章記錄的很多操作都不應該被複製。 深度研究是重倉的許可證,不是看幾篇報告就自動取得的。

五個階段的演進

在 Q4 財報前,NOW 股票在 $145 附近震盪。我選擇賣出 13FEB26 145P,認為股票守得住這個位置。財報後股票急跌,145P 的權利金從 $5.89 跳升至超過 $18,我在 1 月 8 日追加第二手(@ $15.69),兩手合計慘虧:

| 合約 | 賣出 | 買平 | 損益 |

|---|---|---|---|

| NOW 13FEB26 145P(第一手) | $5.89 | $18.54(1/20) | -$1,265(含佣金) |

| NOW 13FEB26 145P(第二手) | $15.69 | $29.66(1/29) | -$1,400(含佣金) |

| 兩手合計 | -$2,665 | ||

這個轉折需要先理解原始的策略設計邏輯:

在建立 NOW 部位之前,我並非純粹的選擇權投機——而是以 「Sell Put 作為預定成本買入股票」 的策略切入:

賣出 145P,收取約 $17 的總權利金

→ 若到期被指派:有效買入成本 = $145 - $17 = $128

→ 若不被指派:賺取全部權利金,等待下一次機會

$128 是這個策略的設計目標成本。 財報後股票急跌至 $114,原本的「被動指派建倉計畫」被強制推前,虧損平倉 Put 並在 $114.87 主動買入現股——反而拿到了比原計畫更低的建倉價。

1 月 29 日同一天完成三個動作:

| 動作 | 細節 | 金額 |

|---|---|---|

| 平倉最後一張 145P | 以 $29.66 買回,確認認賠 | -$2,966 |

| 買入 100 股現股 | @$114.87(低於設計成本 $128) | -$11,487 |

| 立刻賣出 13FEB26 130C | @$6.33,Covered Call 立即啟動 | +$633 |

1 月底買入後,NOW 從 $114 逐步反彈至 $121–$124 區間。我在這段期間積極賣出 Covered Call,並多次 Roll(買回舊合約 + 賣出新合約):

| 合約 | 策略 | 損益 | 說明 |

|---|---|---|---|

| NOW 13FEB26 130C | CC 收租 | +$563.90 | 股票未漲過 $130,完整收取 |

| NOW 06MAR26 115C | CC 收租 | +$86.91 | 小獲利平倉 |

| NOW 20MAR26 112C | CC 滾倉 | +$207.60 | 兩輪操作合計 |

| NOW 20MAR26 130C | CC 收租 | +$221.71 | 高履約價,順利到期 |

| NOW 06MAR26 120C | CC(被迫 Roll) | -$267.10 | 股票漲至 $121,需 Roll |

| NOW 17APR26 110C | CC 滾倉 | -$336.30 | 股票上漲,Call 升值需買平 |

2–3 月的 CC 操作多數成功,有幾次因為股票反彈速度超過預期需要 Roll,但整體收租邏輯清晰。

4 月初市場受到宏觀因素(關稅/政策衝擊)衝擊,NOW 從 $124 快速回落至 $84–$97 區間。面對已持有的 100 股帳面虧損,我選擇逆勢大量加碼:

| 日期 | 買入數量 | 價格 | 累積持股 | 說明 |

|---|---|---|---|---|

| 4月8日 | +16 股 | $97.68 | 116 股 | 第一波接刀 |

| 4月9日 | +24 股 | $90–92 | 140 股 | 繼續加碼 |

| 4月10日 | +60 股 | $84.78 | 200 股 | ⚡ 最大單日加碼,近期低點 |

| 4月22日 | +20 股 | $90.38 | 220 股 | 維持加碼節奏 |

| 4月23日 | +80 股 | $85.04 | 300 股 | ⚡ Q1 財報日,完成建倉 |

加碼的核心邏輯:ServiceNow 的護城河(企業 IT SaaS 黏著度、政府合約、AI Now 平台)在短期宏觀衝擊下並未改變,估值回調至合理區間,是深度研究支撐的買入機會。

4 月大量加碼,背後還有一個關鍵前提:在 Q1 財報(4 月 22 日)之前,我已仔細觀察了 NOW 股票的財報前價量關係。股票雖然在宏觀衝擊下急跌,但在 $84–$85 附近出現了放量支撐、賣壓未見加速的技術型態,顯示籌碼在這個價位有承接力道。

這讓這一波加碼並非純粹押注財報——而是基本面研究(護城河完整)× 技術面確認(價量結構)的雙重驗證。不是「沒有很怕」,而是「有理由不怕」。 財報結果出來之後,訂閱收入、EPS、RPO 全面超預期,更進一步確認了這個判斷的可行性。

📊 ServiceNow Q1 FY2026 財報結果(4 月 22 日盤後)↗

| 指標 | 實際值 | 市場預期 | 結果 |

|---|---|---|---|

| 訂閱收入 | $36.71 億 | $36.5 億 | ✅ 超預期 |

| 總收入年增率 | 22% YoY | 19% | ✅ 超預期 |

| 調整後 EPS | $0.97 | $0.96 | ✅ 超預期 |

| RPO(未完成合約) | $277 億 | — | ✅ +23.5% YoY |

| 2026 全年訂閱收入指引 | $157.4–$157.8 億 | $155.5 億 | ✅ 上調 |

| AI 合約承諾(2026 年) | $15 億 | — | ✅ 材料性成長 |

股票隔日跌 14% —— 因中東局勢(伊朗衝突)導致多筆中東大型合約延後簽約,市場放大負面訊號,無視所有超預期的數據。

財報本質:業務超預期 + 地緣風險引發情緒性殺盤。

4 月 23 日開盤,NOW 因財報後情緒殺盤再跌,我在股票接近前低時買入最後 80 股 @ $85.04,完成 300 股建倉——這是利用市場過度反應的一次主動操作。

同一天,我立刻賣出長天期的 LEAPS Covered Call。選擇在財報後賣出 LEAPS 有兩層邏輯:其一,情緒殺盤拉高了 IV(隱含波動率),賣出時能收到更多時間價值;其二,市場若持續悲觀,LEAPS 的長天期特性讓時間衰退每天持續為賣方工作。

| 合約 | 履約價 | 到期日 | 收到權利金 | 狀態 |

|---|---|---|---|---|

| NOW 17JUL26 85C | $85 | 2026/7/17 | +$935 | 持倉中 |

| NOW 15JAN27 90C | $90 | 2027/1/15 | +$1,548 | 持倉中 |

| NOW 21JAN28 85C | $85 | 2028/1/21 | +$2,764 | 持倉中 |

| 合計(未實現) | +$5,247 | |||

LEAPS 選擇權的時間價值(Theta)遠高於短期合約——一張到期日在 2028 年的 Call,其絕對時間價值高達 $27.64/股($2,764/手)。賣出 LEAPS CC 的邏輯:

① 一次性收取大額權利金,相當於每股降低持有成本 $17–27

② 若股票從 $85 漲回 $90+ 並被 Call 走,仍是微利或平手(相對高成本批的損失縮小)

③ 若股票繼續在低位盤整,時間衰退持續對賣方有利

這是接受「上方空間封頂」以換取「確定性現金流」的策略抉擇。

現有部位全貌

現股持倉

| 批次 | 持股數 | 均價 | 帳面成本 | 說明 |

|---|---|---|---|---|

| 第一批(4月低點) | 150 股 | $85.27 | $12,791 | 4/8–4/10 加碼批 |

| 第二批(較早建倉) | 150 股 | $112.30 | $16,844 | 1–3月建倉批 |

| 合計 | 300 股 | $98.78 | $29,635 |

開放選擇權部位

| 合約 | 方向 | 履約價 | 到期日 | 收取權利金 |

|---|---|---|---|---|

| NOW 17JUL26 85C | 賣出 / Short | $85 | 2026/7/17 | +$935 |

| NOW 15JAN27 90C | 賣出 / Short | $90 | 2027/1/15 | +$1,548 |

| NOW 21JAN28 85C | 賣出 / Short | $85 | 2028/1/21 | +$2,764 |

LEAPS 收取的 $5,247 若計入,每股帳面成本從 $98.78 壓縮至約 $81.28,接近低成本批的水位。

策略思維:這不是計算題,是存活題

這篇文章記錄的不是「我算對了多少」,而是「我在每個關鍵時刻怎麼想、用什麼工具撐過去」。

大多數人面對財報後的急跌,有兩個本能反應:要麼認賠出場,要麼死撐不動。這套策略的核心,是選了第三條路——用工具的多元性主動改變自己的處境。

最初賣 Put,是在對 NOW 的方向下注。財報後急跌,這個賭注輸了。但「認錯」不等於「認輸」——真正的轉折是思維的切換:

把虧損的 Put 部位,理解成「用較高成本取得了一批優質資產的所有權」。從那一刻起,這個部位不再是「需要解決的虧損」,而是「需要經營的資產」。Covered Call 是收租,LEAPS 是鎖定長期現金流,加碼是在低估值時擴大資產規模。每一步都是資產經營的決策。

這套策略之所以能存活,是因為選擇權和現股可以互相轉換、互相補位:

股票跌了? 賣 Covered Call 收租,讓時間替你工作。

IV 暴升? 賣 LEAPS 鎖定高額時間價值,一次性壓低成本。

Put 被迫 ITM? 轉股,把「被動失血」變成「主動建倉」。

低點加碼? 分批現股建倉,配合基本面確認,不是盲目接刀。

這些工具本身不複雜,複雜的是在對的時機選對的工具,而這需要對自己的部位、對公司基本面、對市場結構同時有清楚的認識。

這個策略的邊界在哪裡?

這個五階段策略的成立,有幾個前提條件:

① 基本面必須支撐重倉。 ServiceNow 的持續訂閱收入、AI Now 企業套件的滲透率、自由現金流健康度——這些是讓我敢在 $84 附近大量加碼的底氣。沒有深度研究,攤平就是「越跌越套」。

② LEAPS CC 的上方封頂是真實代價。 若 NOW 在 2028 年前反彈至 $120 以上,這批 LEAPS 合約將限制獲利。這是一個明確的取捨——接受上方空間封頂,換取現在就確認的 $5,247 現金流。

③ 帳戶規模需能承受重倉波動。 300 股 × $85–$98 = 帳面敞口 $25,000–$29,000。這個倉位的波動對小帳戶而言壓力極大,需要有對應的整體部位管理邏輯。

📊 ServiceNow (NOW) v2.1 深度研究:定價權保衛戰

📊 NOW Q1 FY26 財報解析:cRPO 跳指 vs Q2 guide 雜音

📊 NOW 制度化建倉框架 v2.1:三段式方法論

📊 熊市裡先學會活下來:一套散戶也能執行的風控系統

ServiceNow Position Management:

Put Losses → Stock Conversion → Covered Calls → LEAPS

This is not a clean success story. It's a documented evolution — learning from an early mistake, rebuilding with a clearer framework, and ultimately constructing a multi-layer position management system around a high-conviction stock.

ServiceNow (NOW) is the global leader in enterprise IT service management software, with a deep moat in workflow automation and an expanding AI platform. Despite strong fundamentals, the stock carries a high valuation multiple that makes it susceptible to sharp selloffs around earnings and macro events. (→ NOW systematic position-building framework)

📊 Earnings Context ↗

Q4 FY2025 Earnings: ~January 22, 2026 — Heavy options activity in the days before. Stock declined from ~$145 to $114 — the trigger for the strategy reset.

Q1 FY2026 Earnings: ~April 23, 2026 — The same day as aggressive share accumulation and LEAPS covered call sales. The strategy's final chapter for this phase.

Some decisions recorded here — aggressive averaging down, concentrated positions at the lows — may look like undisciplined emotional catching of a falling knife. But there is a context readers can't see: I've been tracking ServiceNow for seven or eight years. Not just reading quarterly earnings, but watching its business cycles, management execution, and moat deepen year over year.

That accumulated understanding gives me a kind of conviction at peak market fear that's difficult to fully quantify. The same logic applies to my positions in CME, CBOE, and IBKR — financial market infrastructure companies I don't just research, but use every day as a practitioner. You understand a business differently when you live inside its product.

Without that foundation, many of the decisions in this article should not be replicated. Deep research is the license for concentration — and it isn't earned quickly.

Phase 1: Naked Short Puts Before Earnings — The Expensive Lesson

Before Q4 earnings, with NOW trading near $145, I sold the 13FEB26 145P at $5.89. After earnings disappointed and the stock fell sharply, I doubled down on January 15 at $15.69. Both positions closed at significant losses:

| Contract | Sold At | Closed At | P&L |

|---|---|---|---|

| NOW 13FEB26 145P (Leg 1) | $5.89 | $18.54 (Jan 20) | ~-$1,265 |

| NOW 13FEB26 145P (Leg 2) | $15.69 | $29.66 (Jan 29) | ~-$1,400 |

| Total | -$2,665 | ||

Selling naked puts into earnings is precisely the wrong setup for an options seller: earnings are Gamma events where a 10% overnight move eliminates all theta advantage and turns Delta into the dominant P&L driver.

Phase 2: The Pivot — From a $128 Target Cost to Stock Ownership

Before understanding January 29, it's important to understand the original intent: the short put was not speculation — it was a planned stock acquisition at $128.

The design: sell the 145P, collect ~$17 in premium, resulting in an effective purchase price of $145 - $17 = $128 if assigned. When the stock fell sharply through $145 post-earnings, the planned assignment became an emergency exit. Closing the puts at a loss and immediately buying shares at $114.87 was not abandoning the strategy — it was executing the stock acquisition at an even better price than the $128 target, accepting the options loss as the cost of the failed execution path.

On January 29, three things happened simultaneously: closed the final 145P at $29.66 (-$2,966), bought 100 shares at $114.87, and immediately sold the 13FEB26 130C at $6.33. The covered call era began that morning.

True cost basis accounting: Including the put losses (-$2,665), the effective cost per share on the initial 100-share position was approximately $141.52 — above the $128 target, but recoverable through systematic covered call writing.

Phase 3: Covered Call Income — Stock Rebounds from $114 to $124

February and March saw NOW recover from $114 to $121–124. I systematically rolled covered calls through this period, capturing time decay across multiple contracts. Best performer: NOW 13FEB26 130C at +$563.90, as the stock didn't reach $130 and the full premium was collected. Several calls required rolling as the stock moved up faster than expected, but the overall CC framework generated meaningful income during the recovery phase.

Phase 4: April Macro Selloff — Aggressive Averaging Down

In early April, macro headwinds (likely tariff-related policy uncertainty) drove NOW from $124 back down to the $84–97 range. This is where fundamental conviction translates into action:

| Date | Shares Added | Price | Cumulative |

|---|---|---|---|

| Apr 8 | +16 | $97.68 | 116 shares |

| Apr 9 | +24 | $90–92 | 140 shares |

| Apr 10 ⚡ | +60 | $84.78 | 200 shares |

| Apr 22 | +20 | $90.38 | 220 shares |

| Apr 23 ⚡ | +80 | $85.04 | 300 shares |

The April 10 purchase of 60 shares at $84.78 represents the tactical low — maximum conviction at maximum fear. The position is now split: 150 shares at a ~$85 average (April tranche) and 150 shares at ~$112 average (earlier tranche).

The aggressive April accumulation wasn't blind averaging down. Before Q1 earnings on April 22, I was closely tracking NOW's pre-earnings price and volume dynamics. Despite the macro-driven selloff, the $84–$85 area showed high-volume support without any acceleration of selling pressure — a technical signature suggesting institutional accumulation at those levels.

This created a double-confirmation framework: fundamental conviction (ServiceNow's moat intact) reinforced by technical structure (price holding on volume). The April buying wasn't fearless — it was informed. When Q1 earnings came in with beats across every key metric, the thesis was validated. The -14% post-earnings drop on the Iran headline was market noise over a fundamentally strong quarter — exactly the kind of dislocation this entire strategy was designed to capitalize on.

Phase 5: Q1 Earnings Drop — Buy the Panic, Sell the IV

📊 ServiceNow Q1 FY2026 Earnings (April 22, After Market Close)

Every key metric beat estimates: subscription revenue +22% YoY to $3.67B (beat), adjusted EPS $0.97 vs $0.96 expected (beat), RPO $27.7B growing 23.5% YoY (beat), full-year guidance raised to $15.74–15.78B. AI-specific contract commitments reached $1.5B for 2026.

The stock dropped 14% on April 23 — driven by disclosure of headwinds from delayed large on-premise deals in the Middle East due to the ongoing Iran conflict. The market amplified one line item into a narrative of demand destruction, ignoring every other beat.

The verdict: a fundamentally strong quarter, punished by geopolitical noise.

On April 23, I bought 80 shares at $85.04 into the post-earnings selloff, completing the 300-share position. Then sold three LEAPS covered calls the same morning — deliberately timing the LEAPS sale to the earnings-elevated IV environment, maximizing the premium received.

The LEAPS covered calls sold on April 23 collected structurally higher premiums precisely because earnings-day implied volatility was inflated. Within days, as the IV crush sets in, the value of those short calls declines — an immediate paper gain for the seller.

| Contract | Strike | Expiry | Premium |

|---|---|---|---|

| NOW 17JUL26 85C | $85 | Jul 2026 | +$935 |

| NOW 15JAN27 90C | $90 | Jan 2027 | +$1,548 |

| NOW 21JAN28 85C | $85 | Jan 2028 | +$2,764 |

| Total LEAPS Premium | +$5,247 | ||

With $5,247 in LEAPS premium received, the effective cost basis on the 300-share position drops from $98.78 to approximately $81.28 per share — close to the April low tranche's cost.

The Real Lesson: This Is a Survival Problem, Not a Math Problem

This article is not a record of how well the numbers worked out. It's a record of how to think — how to survive in a market that moves faster and harder than any model predicts, and how to use the flexibility between options and stock to stay in the game long enough for fundamentals to matter.

Most traders facing a post-earnings drop do one of two things: cut the loss and walk away, or freeze and hope. This strategy chose a third path: use the toolkit's versatility to actively reshape the position.

Selling that initial put was a directional bet on NOW staying above $145. That bet was wrong. But admitting the error didn't mean accepting the loss as the final outcome — it meant changing the frame entirely.

The moment you reframe a losing options position as "I've acquired a stake in a quality asset at a higher-than-ideal cost," everything that follows changes. Covered calls become rent collection. Adding shares at $84 becomes expanding ownership at a discount. Selling LEAPS becomes securing future cash flow. The loss becomes a starting point, not an ending.

Stock falling? Sell covered calls. Let time decay work while you wait.

Implied volatility spiking? Sell LEAPS. Lock in premium at peak fear pricing.

Put going deep ITM? Convert to stock. Turn passive bleeding into deliberate ownership.

Price at generational lows? Add shares in tranches, anchored to fundamental conviction.

None of these tools is complicated in isolation. What's difficult is knowing which tool fits which moment — and having the discipline to switch between them without letting emotion override the framework.

Key Lessons from the NOW Journey

① Don't sell naked puts before earnings — that's a Gamma event, not a theta event. Wait for earnings to pass before establishing positions.

② When a short put goes deep ITM, convert to stock — the put already has a Delta near -1, which means you're already long the stock in economic terms. Converting locks the entry price and activates the covered call income mechanism.

③ Averaging down requires fundamental conviction, not hope — the April accumulation only makes sense because ServiceNow's moat (enterprise contract stickiness, government integrations, AI Now platform) remained intact despite the macro selloff.

④ LEAPS covered calls are a structural tool, not a trade — selling $27/share in time value on a 2028 LEAPS is not about predicting the stock's price by then. It's about mathematically compressing your cost basis by accepting a defined ceiling on your upside.

Comments ()