從裸賣 Put 到垂直價差:2026 Q1 操作風格演進實錄

從裸賣 Put 到垂直價差的真實操作演進。在川普關稅高波動環境下,以彈性出場原則操作 ALAB、CF、FN、GDX、ETN、NET 六個標的,13/13 垂直價差全勝,ALAB 裸賣 Put 單筆 -$758 是觸發風格轉變的直接原因。

從裸賣 Put 到垂直價差的真實操作演進。ALAB -$758 的一次教訓,觸發了操作風格的根本改變。

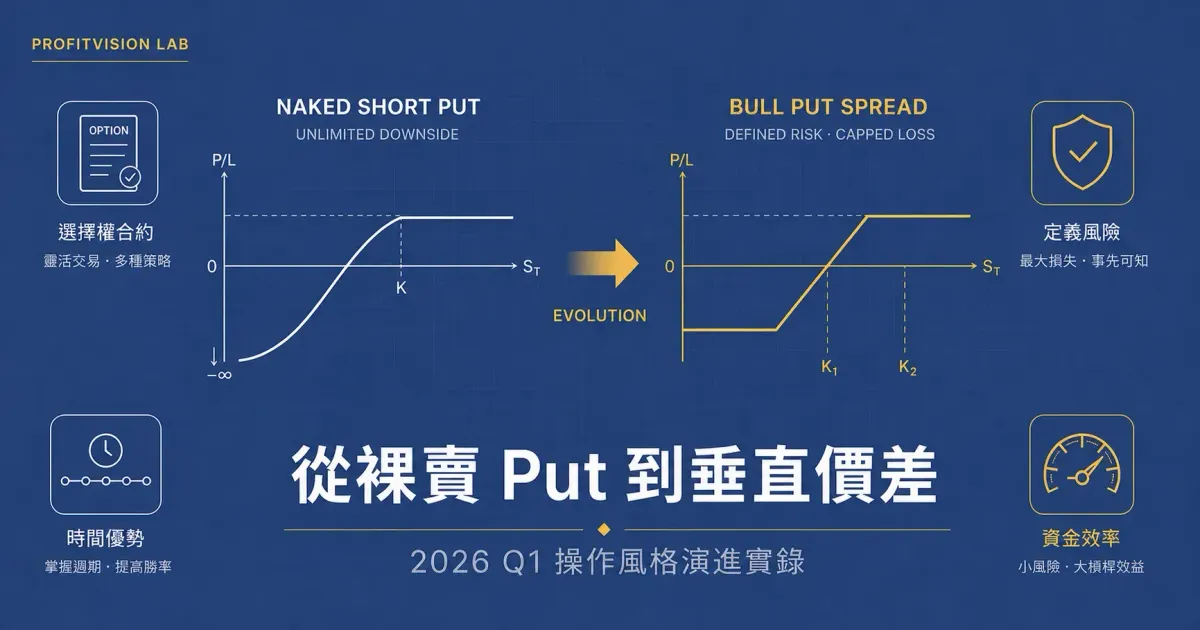

選擇權賣方策略有兩種截然不同的形態:一種是裸賣 Put(Naked Short Put),理論上承受無限下方風險;另一種是垂直價差(Vertical Spread),透過同時買入一張保護性 Put,將最大損失鎖死在一個已知的數字之內。

這篇文章記錄了我在 2026 年第一季的操作風格轉變——從 1 月的裸賣 Put 模式,逐步演進為 3 月後以垂直價差為主的操作框架——並用六個真實案例(ALAB、CF、FN、GDX、ETN、NET)說明這個轉變的過程與成效。

裸賣 Put vs. 垂直價差:核心差異

❌ 裸賣 Put(舊做法)

- 只賣出一張 Put,無保護

- 收到較高的權利金

- 下方風險理論上無限

- 若股票崩跌,損失可能遠超預期

- 佔用大量保證金(Cash-Secured)

✅ 垂直價差(新做法)

- 賣出高履約價 Put + 買入低履約價 Put

- 收到的淨權利金較少

- 最大損失 = 價差寬度 - 淨權利金

- 無論股票崩多深,損失有上限

- 保證金需求低,資金效率高

第一階段:ALAB 裸賣 Put(2026 年 1–2 月)

ALAB(Astera Labs)是 2025–2026 年 AI 基礎設施題材中波動最劇烈的半導體股之一。1 月初,股票仍在高位震盪,我選擇以裸賣 Put 策略收取時間價值。

成功的一面:靈活滾倉

在 1 月 6 日至 1 月 12 日之間,我對 13FEB26 145P 進行了兩輪操作,每一次都是快速進出,成功收取時間衰退:

| 合約 | 動作 | 時間 | 損益 | 說明 |

|---|---|---|---|---|

| ALAB 13FEB26 145P(第一輪) | 賣開→買平 | 1/6–1/7 | +$443 | 股票小幅反彈,快速獲利 |

| ALAB 13FEB26 145P(第二輪) | 再賣→再平 | 1/7–1/12 | +$189 | 繼續收割時間衰退 |

| ALAB 20MAR26 140P | 賣開→買平 | 2/6–2/9 | +$311 | 股票回升,順利平倉 |

代價:一次爆倉的教訓

1 月 5 日,我賣出了 ALAB 06FEB26 160P,履約價接近當時的市場價格,Delta 偏高。隔天,ALAB 跳空大跌,160P 的權利金從 $10.67 跳漲至 $18.25,我被迫認賠出場:

| 合約 | 賣出 | 買平 | 損益 | 說明 |

|---|---|---|---|---|

| ALAB 06FEB26 160P | $10.67 / 手 | $18.25 / 手 | -$758 | 跳空下跌,Delta 過高被燙到 |

裸賣 Put 最怕的不是緩慢下跌,而是跳空缺口(Gap Down)。ALAB 這次跌幅超過 8%,完全越過了履約價,讓時間衰退的優勢瞬間歸零,反而變成 Delta 的受害者。若當初有買入保護腳(long put),最大損失就能被事先鎖定。

轉折點:3 月起全面轉向垂直價差

2 月底至 3 月初,我開始將新增部位全部改為垂直價差結構。這個改變帶來的不是更高的絕對報酬,而是更可預測的風險上限。以下是 2026 年 3–4 月的六個垂直價差案例:

2026 年第一季的市場環境極為特殊:川普政府的關稅政策反覆無常,市場情緒在短時間內劇烈擺盪。在這樣的環境下,我對垂直價差的獲利目標採取了彈性出場原則——沒有死守「等到 50% 最大獲利才平倉」的教科書規則。

有時市場突然反彈,達到 20% 目標獲利就果斷出場鎖利;有時股票在支撐位站穩、波動率下降,才持倉等到 50%。這背後有清晰的實務邏輯:

① 浮盈不是真盈。 在高波動市場裡,今天的 +30% 浮盈,明天一個關稅公告可能立刻變成 -20%。20% 落袋為安,是保住已賺到的錢,不是放棄獲利。不要跟錢過不去。

② 資金效率的乘數效應。 平倉後資金立刻釋放,可以立刻尋找下一個機會。死守一個 30% 浮盈的部位等 50%,不如平倉後再開一個新的高勝率價差。一季下來,多做幾筆比每筆做滿更重要。

③ 彈性才是這個環境下的紀律。 不是沒有規則,而是規則本身就包含「視市況調整出場時機」這一條——川普投顧太難猜了,機械式地死守目標反而是把主動優勢拱手相讓。

案例一:CF Industries(CF)— Bull Put Spread

CF 是美國主要氮肥生產商,業務與農業週期高度相關,股價波動相對可預測。我選擇 Bull Put Spread,在技術支撐下方設置雙腳防禦。

| 到期日 | Short Put | Long Put | 開倉日 | 平倉日 | 損益 |

|---|---|---|---|---|---|

| 17APR26 | $120(賣出) | $115(買入) | 3/12 | 3/27 | +$22.90 |

| 18JUN26 | $105(賣出) | $100(買入) | 4/17 | 4/23 | +$128.77 |

合計:+$151.67 — 兩輪操作全勝,最大損失均被鎖定在 $5 價差寬度內。

案例二:Fabrinet(FN)— 高股價垂直價差

FN 是光纖元件代工龍頭,股價高達 $490–$590,操作一般選擇權合約的資金需求極高。改用垂直價差後,保證金需求大幅降低,且每筆交易的最大損失清晰可見。(→ FN 基本面護城河深度研究)

| 到期日 | Short / Long Put | 開倉 | 平倉 | 損益 | 結果 |

|---|---|---|---|---|---|

| 17APR26 | $530 / $520 | 3/3 | 3/10 | +$115.60 | 獲利 |

| 15MAY26(第一輪) | $440 / $430 | 3/17 | 3/20 | +$41.10 | 獲利 |

| 15MAY26(第二輪) | $480 / $470 | 3/26 | 3/27 | +$72.40 | 獲利 |

| 15MAY26(第三輪) | $450 / $440 | 3/30 | 4/8 | +$49.30 | 獲利 |

| 18JUN26 | $590 / $580 | 4/16 | 4/23 | +$30.80 | 獲利 |

FN 合計:+$309.20 — 五輪全勝,展現了垂直價差在高股價標的的應用潛力。

案例三:GDX(黃金礦業 ETF)— 多頭價差搭順風車

2026 年 3 月,黃金受到避險需求帶動強勁上漲,GDX 同步走強。我在技術確認趨勢後,以 Bull Put Spread 做多,履約價設在支撐位下方:

| 到期日 | Short Put | Long Put | 操作期間 | 損益 |

|---|---|---|---|---|

| 15MAY26 | $75(賣出) | $70(買入) | 3/20–3/23 | +$24.50 |

單輪操作,持倉僅 3 天即獲利出場。定義好最大損失($500 - 淨權利金)後,心理壓力顯著降低。

案例四:Eaton(ETN)— 工業股防禦型價差

ETN 是工業電氣龍頭,基本面穩健。3 月中旬市場震盪期間,我以垂直價差在技術支撐 $330 下方建立緩衝:

| 到期日 | Short Put | Long Put | 操作期間 | 損益 |

|---|---|---|---|---|

| 01MAY26 | $340(賣出) | $330(買入) | 3/16–4/8 | +$146.00 |

案例五:Cloudflare(NET)— 雲端股 4 月反彈操作

4 月中旬市場出現技術反彈訊號,我選擇 NET(Cloudflare) 以 Bull Put Spread 參與:

| 到期日 | Short Put | Long Put | 操作期間 | 損益 |

|---|---|---|---|---|

| 18JUN26 | $160(賣出) | $150(買入) | 4/14–4/16 | +$57.46 |

2026 Q1 垂直價差成績單

相比之下,裸賣 Put 時期(ALAB 1–2 月)單筆最大虧損 -$758,而整體獲利需靠多次成功交易積累才能彌補。

結論:紀律不是關於獲利多少,而是風險是否已知

垂直價差不是更賺錢的工具,而是更可管理的工具。它的核心價值在於:

① 進場前就知道最壞情況 — 不會有「以為只虧一點,最後虧一大筆」的意外

② 保證金需求降低 — 相同資金可以同時持有更多不相關的部位,分散風險

③ 心理壓力可量化 — 當你知道最大損失是 $500,你能用平靜的心態等待時間衰退

ALAB 160P 的 -$758 單筆損失,超過了後續所有垂直價差的總獲利。這個對比,是促成風格轉變最直接的原動力。

📊 Fabrinet (FN) 深度研究:AI 光通訊隱形冠軍護城河

📊 GDX 金礦 ETF:當個股全卡關,用 Bull Put Spread 管理板塊風險

📊 Cloudflare (NET) Top-Down 深度研究報告

📊 AI 成長股怎麼「邊持有邊收租」?以 TTD 為例的三層期權策略教學

Comments ()